UPDATE: Ouch! How much will UST debt service go up when Fed Funds get bumped?

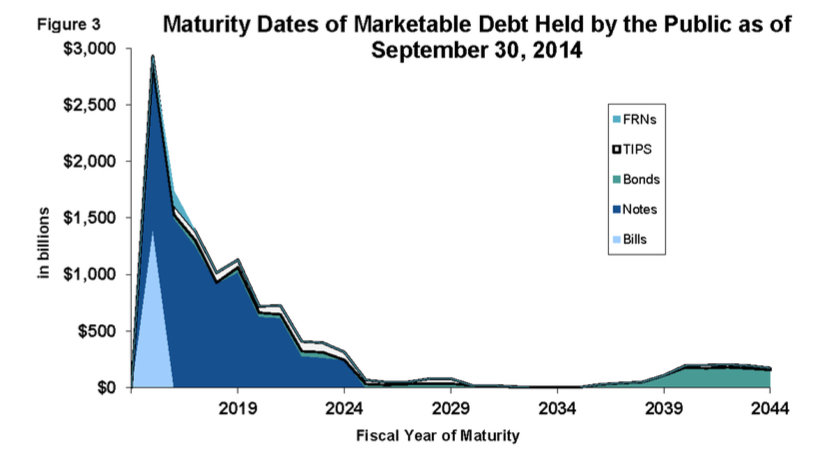

The U.S. Treasury debt is fairly short in duration (see the graph below). When interest rates move up, what will happen to the cost of servicing the debt?

UPDATE June 11:

An article in today’s WSJ (link for subscribers) notes, “An extended surge in yields could jeopardize growth as it would lead to higher borrowing costs for consumers and businesses.” Unmentioned in the article and undiscussed by the Fed in the elephant in the index–sorry, I meant the elephant in the room: the enormous and short-duration U.S. Treasury debt. A surge in yields will create a surge in debt service, and additional demands for either more borrowing or more taxes to simply service the existing debt. The FOMC seems to be doing a better job of helping to manage the fiscal challenges than Congress–so it would seem they are aware of this and will be reluctant to ratchet rates too far because of the flow through effects on the economy.

When rates begin to move, as maturing debt is rolled over, the debt service costs will start to move almost immediately. What if short rates move 100 basis points? How about 200 basis points? Due to the short duration profile of the debt, an increase in short term rates will begin to affect debt service costs very quickly. What will the increase in debt service costs do to the already negative Federal budget? Borrow more? Raise taxes? What will be the impact on the (fragile) economy? And to stocks?

Chart is from Treasury Direct, GAO-15-157 Schedules of Federal Debt, Page 19. Note also that this is only the marketable debt–it excludes the $5 trillion+ (as of 9-30-14) of Intergovernmental Debt Holdings.

This does not lead me to suggest that bonds should be avoided–but that investors with an appropriate weighting in bonds should be cautious in selecting maturity dates. This is a topic that has not received any attention yet. My guess is that it will start getting headlines about 30 minutes after the next Presidential election.

Comments? What do you think?