Welcome to Pat Luby’s Muni Catchup for June 27

Welcome to Pat Luby’s Muni Catchup for June 27

This week’s ingredients:

- Introducing a New Weekly Feature: Wisdom from Buffett

- I Told You So, Part 1

- Puerto Rico: Caveat Emptor

- Demand Side: Flows

- Demand Side: Redemptions

- I Told You So, Part 2

- The Bottom Line

- The Declaration of Independence

Introducing a new weekly feature: Wisdom from Buffett

For the summer, I am adding a new weekly feature in the Muni Catchup, “Wisdom from Buffett.” His insights and stories about how he has approached life have endeared him to his fans. And, because his timeless wisdom appeals to young and old alike, he seems to be more influential and popular than ever. I have always been impressed by how well he is able to express himself, which is why–as my family knows–I simply refer to him as The Poet. Please let me know what you think of this new feature.

Wisdom from Buffett

And there’s that one particular harbour

Sheltered from the wind

Where the children play on the shore each day

And all are safe within

Most mysterious calling harbour

So far but yet so near

Jimmy Buffett, “One Particular Harbor”

I Told You So, Part 1:

Brexit, brexit, brexit.

Are you sick of hearing about it already? You can’t say I didn’t warn you! Here’s what I wrote in last week’s Catchup:

Brexit is going to be all over the news this week and has the potential to send ripples across all the markets around the world…even the muni bond market.

Perhaps not as much because of the immediate market reaction (which could affect currency and bond markets), but because of the long-term implications.

I write not as an economist, but as a student of the markets and an interested observer of the economy. Should the UK leave the EU, it would reduce the likelihood of the Euro ultimately achieving equal status with the dollar as a reserve currency, and it is the exclusive status as the world’s currency that has allowed many of the U.S. fiscal and monetary policies that–in my view–have added friction to the economy and reduced growth, with obvious implications for the bond markets and interest rates.

If the UK exits the EU, that could be bullish for the U.S. dollar, and push our interest rates lower–as we have seen over just the last two weeks. Some of this seems to be already priced into the markets…but is there more? What happens if the vote is to stay in? Will some of the recent rally unwind? Currency markets are large and liquid, and when money moves to a “safe haven,” it is often put into the bond markets–that is why muni bond investors should be paying attention to the Brexit vote. Investors have been waiting for years for yields to “go back up,” but there are forces that could actually push yields lower.

So to answer my own question about how much of the vote was already priced into the bond market, not much! Investors around the world sought out the safe harbour of the U.S. bond market, driving yields down, even in the muni market.

S&P Dow Jones publishes 206 muni market indices, and on Friday, only one of them was down. (The Puerto Rico G.O. Bond Index, which was off 1.8% on the day, although for the month it is up 1.6%) The champ was the S&P Muni Bond 20-Year High Grade, which was up 1.98% on the day! Take a look at the MTD and YTD returns:

Of course, no one expected the kind of rally like we saw on Friday, but it is a good reminder that low yields ≠ low returns. (Well, they don’t have to equal low returns, but there’s no symbol for “does not always equal.” I’ve written about this before.) For investors on the sideline, Friday’s rally did nothing for their YTD total return, but this is not to suggest that long-term investors should be jumping in at this pont either. Price action like this is caused by the flight of capital to the safe harbour and when the market conditions normalize, the harbour will empty out as capital goes back out to get back to work.

For more comments about the market, see The Bottom Line, below, and for end-of-the-week data go to the Muni Market Yields in Context page.

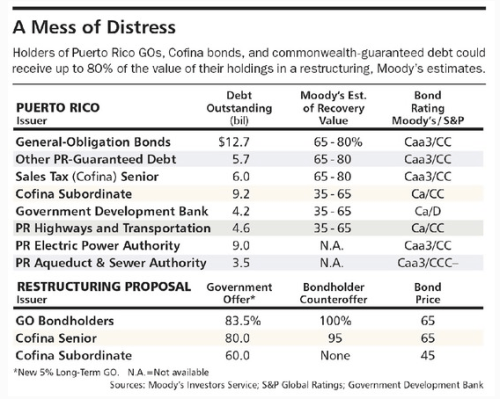

Puerto Rico: Caveat Emptor

This week’s issue of Barron’s (June 27 issue) has a good update on Puerto Rico munis and includes some interesting projections from Moody’s of recovery rates for some of the Puerto Rico debt. (See below for the table, but I encourage you to read the entire article.)

The article suggests that “For investors bullish on Puerto Rico’s prospects, the best bet is its $12.7 billion of general-obligation bonds—plus some $5.7 billion of less-liquid commonwealth-guaranteed debt.”

The word omitted in the article is “speculative.” Uninsured Puerto Rico bonds are non-investment grade, also called junk and formerly known as “speculative grade.” I have always preferred the term “speculative” because it is an explicit reminder that something has to change for the issuer to be able to pay their principal and interest. It is not just that there is a low or zero margin of safety–there is a negative margin of safety. In the case of Puerto Rico, there is still much uncertainty about how that gap will be closed–and how much of it will come from bondholders accepting a haircut.

This will be a noteworthy week for Puerto Rico, with the Senate expected to approve a Federal oversight board in advance of Friday when a $2 billion debt service payment is due. So IF one is bullish on Puerto Rico and one wants to act on that, keep in mind that it would be a speculative investment. (My suggestion would be that for investors interested in this type of muni, an actively managed high yield muni bond fund is an excellent way to get that exposure in a widely diversified and professionally managed and supervised portfolio.)

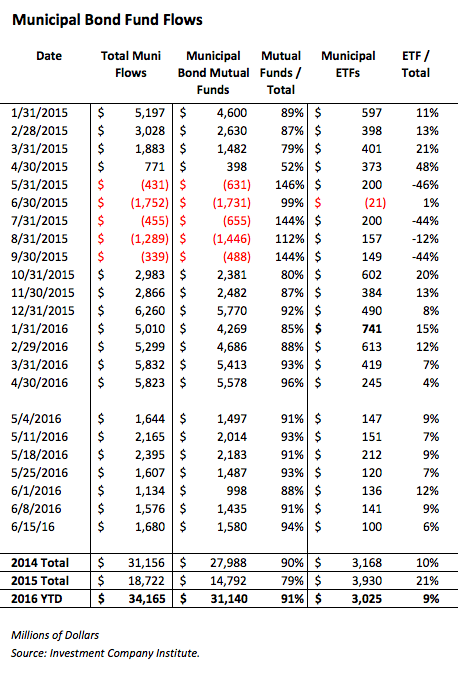

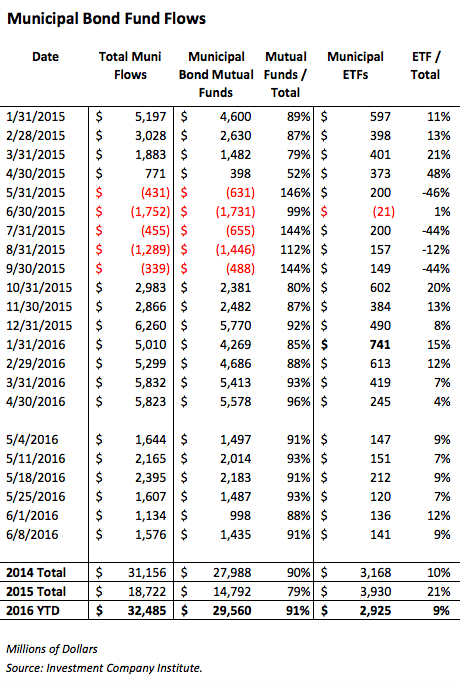

Demand Side: Fund Flows Remain HUGE!

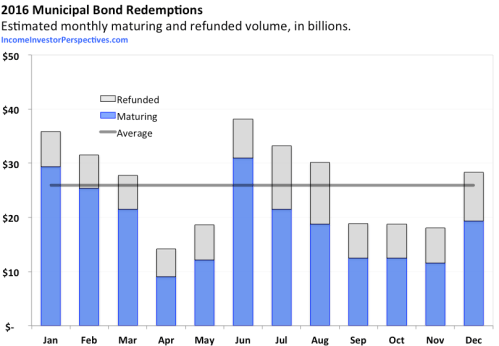

Demand Side: More Redemptions Coming!

$33.2 billion–that’s the estimate for the volume of munis maturing in July. Way above this year’s estimated monthly average of $26 billion. Through May, based on data from SIFMA, the muni market has averaged $34.7 billion in new issue volume.

If every matured dollar needs to get reinvested, and fund flows continue to be heavy, it could be hard to find good bonds with good structure at a reasonable price. With the huge post-Brexit runup in prices, dealers will be forced to mark up their offerings, so I would not be surprised to see buyers wait a little bit to let the market settle in at the new yield levels.

See Summer Redemption Season for the breakdown of redemptions by state. As I have noted before, I am never in favor of trying to time interest rates, so if you have bonds getting redeemed and you are reluctant to lock up the principal, you may wish to consider using muni ETFs as a liquid way to at least serve as a placeholder in munis to maintain your exposure. You can use a short duration ETF to maintain exposure without taking on too much interest rate risk in case yields move against you. My article on ETF.com offers a Guide to How to Pick the Right Muni ETF. By the way, I still like the idea of using taxable muni ETFs in accounts that do not need the tax exemption. Click here to read that article.

I Told You So, Part 2:

Last summer, rather than offering the world another reading list, I published my Summer Thinking List to help readers prepare for the back-end of the year. It was one of my most popular posts of the year, and included a then timely question:

Do my muni mutual fund clients have exposure to Puerto Rico? Is action needed?

Is there something on this year’s list as prescient? We’ll have to wait until next year to decide, but you’ll be able to see this year’s list soon…it will be published later this week.

New this year is that the list has been split into two editions: one for advisors, and a very different one for investors. The theme of the Investor version is, “Am I prepared for retirement?” Advisors are encouraged to share the investor’s list with clients and prospects. Both versions will be available as web pages and as PDFs. If you still haven’t signed up to receive notifications of my articles when they get published, do yourself a favor and do it right now.

Summer at Lake Winnipesaukee. Sitting in that chair would be a great spot to be reading the Summer Thinking List! (Photo by the author.)

The Bottom Line

U.S. bond market yields have been distorted by the flows coming in as a result of the mostly unexpected Brexit vote.

As details emerge about the post-Brexit circumstances in England and Europe, capital will leave the U.S. bond market to be put back to work elsewhere–thus allowing yields to presumably move higher. That could be a very slow process, however. It is impossible to know how long it will take. Will it be Monday? September? Next year? My expectation is that first some clarity from the EU will be needed, and then there is the election in England in October and the U.S. election in November. There would seem to be sufficient reason for much of the temporary flows into bonds to err on the side of caution and remain in U.S. bonds until the results of both elections are known.

Investors with a long-term perspective should not feel the need to jump in if they have been underallocated, but neither should they allow themselves to be underallocated versus their plan. Clearly, uncertainty remains, meaning that rates could go down further. It is possible for investors to maintain an appropriate exposure to fixed income while underweighting their exposure to duration or credit risk. Premium bonds and especially premium non-callable bonds may be a good way to gain lower risk market exposure.

The Unanimous Declaration of the Thirteen United States of America, Adopted in Congress 4 July 1776

When was the last time you sat down and read our country’s founding document? Independence Day is a good time to do that. My old friend John Murfee is in the habit of reading it out loud for his family and friends before the traditional dinner of hamburgers and hot dogs is served. Do you have a similar tradition? I’d like to hear about it!

When, in the course of human events, it becomes necessary for one people to dissolve the political bonds which have connected them with another, and to assume among the powers of the earth, the separate and equal station to which the laws of nature and of nature’s God entitle them, a decent respect to the opinions of mankind requires that they should declare the causes which impel them to the separation.

We hold these truths to be self-evident, that all men are created equal, that they are endowed by their Creator with certain unalienable rights, that among these are life, liberty and the pursuit of happiness. That to secure these rights, governments are instituted among men, deriving their just powers from the consent of the governed. That whenever any form of government becomes destructive to these ends, it is the right of the people to alter or to abolish it, and to institute new government, laying its foundation on such principles and organizing its powers in such form, as to them shall seem most likely to effect their safety and happiness.

Click here for a 2-page PDF of the Declaration of Independence.

More Catchup

More Catchup

The next regular Muni Catchup won’t be published until after the Fourth of July. However, on Friday I plan to publish a quick note with some of the quarter-end data. If you will be out on Friday, then I extend to you my very best wishes for a safe and fun celebration of our nation’s birthday.

By the way, your comments and questions are always welcome and appreciated. What do you like about the Muni Catchup? What would make it more helpful for you? Let me know!

Thanks for reading,

Pat

The opinions expressed and the information contained herein are based on sources believed to be reliable, but accuracy or appropriateness is not guaranteed. Past performance is interesting but is not a guarantee of future results. Investments in bonds are subject to gains/losses based on the level of interest rates, market conditions and credit quality of the issuer. Indices are not available for direct investment, although in some cases, there may be ETFs available designed to track some of the indices shown. The author does not provide investment, tax, legal or accounting advice–this is not investment advice. Investors should consult with their own advisor and fully understand their own situation when considering changes to their strategy, tactics or individual investments. Additional information available upon request.

©2016 Patrick F. Luby

All Rights Reserved

Above: summer at Lake Winnipesaukee. It looks pretty darn nice, doesn’t it? Is that person in the chair reading The Summer Thinking List?

Above: summer at Lake Winnipesaukee. It looks pretty darn nice, doesn’t it? Is that person in the chair reading The Summer Thinking List? Welcome to the Muni Catchup! It’s now official–today is the first day of summer. Around here, it has felt like summer for several weeks. In past years, markets got slower and quieter in the summer, but not anymore–and this week is not going to be a quiet or slow week.

Welcome to the Muni Catchup! It’s now official–today is the first day of summer. Around here, it has felt like summer for several weeks. In past years, markets got slower and quieter in the summer, but not anymore–and this week is not going to be a quiet or slow week.

That means that we can stop waiting for the Fed, and get back to the business of investing, right? Before I answer that question, let me quote from one of my

That means that we can stop waiting for the Fed, and get back to the business of investing, right? Before I answer that question, let me quote from one of my  The opinions expressed and the information contained herein are based on sources believed to be reliable, but accuracy or appropriateness is not guaranteed. Past performance is interesting but is not a guarantee of future results. Investments in bonds are subject to gains/losses based on the level of interest rates, market conditions and credit quality of the issuer. Indices are not available for direct investment, although in some cases, there may be ETFs available designed to track some of the indices shown. The author does not provide investment, tax, legal or accounting advice–this is not investment advice. Investors should consult with their own advisor and fully understand their own situation when considering changes to their strategy, tactics or individual investments. Additional information available upon request.

The opinions expressed and the information contained herein are based on sources believed to be reliable, but accuracy or appropriateness is not guaranteed. Past performance is interesting but is not a guarantee of future results. Investments in bonds are subject to gains/losses based on the level of interest rates, market conditions and credit quality of the issuer. Indices are not available for direct investment, although in some cases, there may be ETFs available designed to track some of the indices shown. The author does not provide investment, tax, legal or accounting advice–this is not investment advice. Investors should consult with their own advisor and fully understand their own situation when considering changes to their strategy, tactics or individual investments. Additional information available upon request.