Muni Catchup: FOMC Edition

by PL

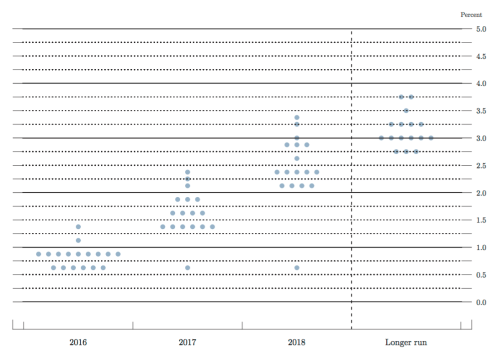

The new dot plot is here! The new dot plot is here!

That means that we can stop waiting for the Fed, and get back to the business of investing, right? Before I answer that question, let me quote from one of my earlier comments on the Dot Plot:

That means that we can stop waiting for the Fed, and get back to the business of investing, right? Before I answer that question, let me quote from one of my earlier comments on the Dot Plot:

Short-term interest rates are influenced first and foremost by monetary policy. So if you want to know where rates are going–and when–you would want to know what the members of the FOMC are thinking. Right? They’re in the driver’s seat, with their collective foot on the gas pedal or the brake.

But even the members of the FOMC are not of one opinion about the magnitude of future changes in rates…that’s what I find most interesting about the chart.

Midpoint of Target Range for Fed Funds Rate (in percent):

| Dec 31, 2016 | Dec 31, 2017 | Dec 31, 2018 | Beyond | |

| Range | 5/8 to

1 3/8 |

5/8 to

2 3/8 |

5/8 to

3 3/8 |

2 ¾ to

3 3/4 |

| Average | .82 | 1.57 | 2.46 | 3.14 |

| Median | 7/8 | 1 5/8 | 2 3/8 | 3 |

So which forecast is correct? Are any of them correct? Paying attention to the Fed is important, but long-term investors should have a different take-away than traders and economists. If you have money to put to work (say, from your munis that matured June 1), then trying to forecast rates can easily backfire on you. Here’s what Alan Greenspan had to say about forecasting rates:

I think forecasting markets is very difficult, I would argue at the end of the day, probably with rare exceptions, almost impossible. But what you can do is measure the risks. And the risks essentially are different from somebody who is 30 years old and is saving for retirement or one who is 55. And I think those types of judgments are crucial and important for appropriate investment policies for retirement, and I don’t think you can generalize very far down the road. (Alan Greenspan, speaking as Chairman of the Federal Reserve, April 30, 2003.)

I’ll quote again from one of my earlier posts:

Waiting for higher rates remains very popular. However, by trying to time rates and underallocating to bonds, investors may unwittingly be taking on more risk by missing out on the diversification benefits of holding bonds with their stocks. We believe it is unwise to try to time interest rates, and suggest instead to mitigate the risks of a rising rate environment by adjusting within fixed income (which specific investments you own), rather than shifting your asset allocation. Click here to read more about timing rates.

Bottom line: unless you are smarter than an FOMC’er, let your investment policy determine your asset allocation. Your view of market conditions and trends should influence which investments you select–not whether or not you remain invested.

So to answer my earlier question, yes–it is time to get back to the business of investing. That doesn’t mean that you should ignore the market environment, but that you should take account of it and make the best decision possible. I’ll be back on Thursday with an update of my interest rate chart from Monday’s Catchup.*

Thanks for reading,

Pat

*What? You did SEE Monday’s Catchup? Then go subscribe right now so that you don’t miss any more. The sign-up box is below.

The opinions expressed and the information contained herein are based on sources believed to be reliable, but accuracy or appropriateness is not guaranteed. Past performance is interesting but is not a guarantee of future results. Investments in bonds are subject to gains/losses based on the level of interest rates, market conditions and credit quality of the issuer. Indices are not available for direct investment, although in some cases, there may be ETFs available designed to track some of the indices shown. The author does not provide investment, tax, legal or accounting advice–this is not investment advice. Investors should consult with their own advisor and fully understand their own situation when considering changes to their strategy, tactics or individual investments. Additional information available upon request.

The opinions expressed and the information contained herein are based on sources believed to be reliable, but accuracy or appropriateness is not guaranteed. Past performance is interesting but is not a guarantee of future results. Investments in bonds are subject to gains/losses based on the level of interest rates, market conditions and credit quality of the issuer. Indices are not available for direct investment, although in some cases, there may be ETFs available designed to track some of the indices shown. The author does not provide investment, tax, legal or accounting advice–this is not investment advice. Investors should consult with their own advisor and fully understand their own situation when considering changes to their strategy, tactics or individual investments. Additional information available upon request.

©2016 Patrick F. Luby

All Rights Reserved

[…] Please read this in conjunction with Wednesday’s FOMC Edition. […]

LikeLike