Muni Catchup 7/25

This week in the Muni Catchup:

- Fiduciary, Munis & You

- Should All Munis Be Taxable? Part 2

- Redemptions

- Wisdom from Buffett

- Summer Reminder

- The Bottom Line

Fiduciary, Munis & You

Because most investors do not buy munis in their tax-deferred retirement accounts, municipal bond market participants may not have been paying close attention to the new Department of Labor fiduciary rule, which applies only to retirement accounts. However, a recent article in Investment News shows that the Department of Labor has been paying attention to the muni market, as shown by a recent clarification to the rule:

Originally, firms acting as principals would have been prohibited from directly purchasing and selling muni bonds from or into a client’s retirement account. The April version of the rule was changed to allow principals, which hold muni bond inventories, to purchase bonds from clients, essentially expanding the market of potential buyers of the bonds.

This is good for investors. The DOL clearly recognized that, particularly in times of market stress, there is no logical upside to limiting the universe of potential buyers of a security that an investor wants to sell.

However, for some reason, the DOL seems to be holding firm, for the time being, on not allowing principals to sell muni bonds out of its inventory to clients investing through their individual retirement accounts.

Jeff Benjamin, DOL fiduciary rule gets it half right on the municipal bond market. InvestmentNews, July 7, 2016.

This would seem to be irrelevant to the muni market because munis are rarely purchased in tax-deferred accounts. In practical terms, though, it is relevant for taxable munis (such as Build America Bonds), because they often offer higher yields than are available on comparably rated corporate bonds–making them attractive for purchase in retirement accounts.

Because the rule will disrupt how dealers will be able to re-distribute the bonds purchased from retirement accounts, the current equilibrium in the already illiquid taxable muni market may be upset, forcing yields (and yield spreads) higher to offset the reduction in potential demand.

Taking advantage of those higher yields may be more difficult, though, because of the coming changes in how market makers will be able to transact with retirement accounts. Rather than buying individual bonds, however, financial advisors and investors may find it easier to buy and manage their allocation to taxable munis by using mutual funds or ETFs.

Investors with tax-exempt portfolios, such as endowments and foundations, may an even more attractive opportunity since they will retain the ability to transact directly with the market makers.

Footnote: InvestmentNews has a page dedicated to their coverage of the DOL fiduciary rule.

Should All Munis Be Taxable? Part 2

As I explained in my special Catchup last week, it is not me asking that question, but it is the topic of a new research report published last week by The Tax Foundation. In addition to what I wrote last week, I had one more thought to share:

- If Congress did move to reduce or eliminate the tax exempt status of munis, would that also prompt a move by the states to seek the ability to tax interest income from U.S. Government and Agency bonds?

You may also wish to read this article from Bloomberg about the potential for increased political risk to the tax-exemption from a narrowing investor base.

Redemptions

Yes, Christmas is just five months away, but right now it is DEFINITELY still summer. The forecast high for today in my town was 99 degrees…which, as you can see, is hotter than another well-known place…

Yes, Christmas is just five months away, but right now it is DEFINITELY still summer. The forecast high for today in my town was 99 degrees…which, as you can see, is hotter than another well-known place…

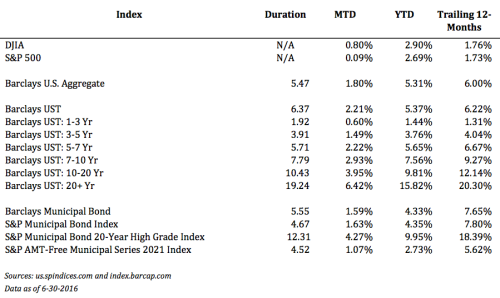

Meanwhile, in the air-conditioned comfort of the muni market, it is still Summer Redemption Season, which will conclude in August as an estimated $30.1 billion in redemptions will flow back to investors.

At current rates, many advisors and investors are be uncertain about how to reinvest–or even if they will want to reinvest in municipal bonds.

In addition to all of the factors that should normally be considered (issuer, credit rating, coupon rate, maturity date, call features, par amount, etc.), the decline in secondary market liquidity and the increase in political risk need to be managed more carefully than ever. See The Bottom Line, below, for my current thinking.

The Wisdom of Buffett

There are only a few more weeks of summer, which means only a few more installments in my “Wisdom from Buffett” series. It is especially in summer when I find that his insights and stories really resonate with me, but his timeless wisdom transcends seasons and appeals to young and old alike. I have always been impressed by how well he is able to express himself, which is why–as my family knows–I simply refer to him as The Poet.

This week’s quote:

When I woke up this morning

I was tired as I could be

I think I was counting my money

When I should have been counting sheepFrom Makin’ Music for Money, by Jimmy Buffett

Summer Reminder

What are you reading this summer?

To help you “digest” what you read this summer, be sure to also spend some time with The Summer Thinking List. This year’s edition is already my all-time most viewed post.

There are separate versions for advisors and investors, but don’t wait! Once Labor Day gets here, the lists will be taken down and put away until next summer.

The Bottom Line

Check Your Calls: Older callable bonds that are valued at a premium are at an increased risk of being called away–just as the reinvestment options have become less attractive. This doesn’t mean that you should sell callable bond holdings, but it does mean that you should only add additional callable premium bonds after evaluating the concentration of call risk in your portfolio. It would also be sensible to evaluate what you would do if your callable bonds were called at their next call date.

Beware the Coupon: Favoring par bonds now may not be a prudent move for investors because of the potential exposure to the unfavorable tax treatment on market discount should rates move higher. If you are a buyer, continue to favor premium bonds–to reduce the risk of bonds moving to a discount if rates move higher.

Pay Attention to Duration, but Don’t Be Afraid of It: As uncertainty clears and some of the recent global flows into bonds reverses, higher duration bonds and indices will be expected to underperform the rest of the bond market. So while it may be tempting to put new money to work where performance has been the strongest (in long-duration bonds, funds or ETFs), we all know that past performance is not an indicator of future returns. When the market turns, duration will be the total return investor’s foe. Unless you are an active total-return investor prepared to react quickly to market changes, new money should be put to work in line with the long-term goals as defined by your investment policy statement. But don’t be afraid of duration…it is possible to be too short on the yield curve. My discussion of duration in this article also applies to mutual fund and bond selection.

Don’t Forget Taxable Munis! Investors with money in tax-deferred or other non-taxable accounts should compare the yields on taxable muni bond offerings versus comparably rated corporate bonds. But as I noted above (in Fiduciary, Munis & You), it is now time to be paying attention to how you buy taxable munis–especially in tax-deferred retirement accounts.

Thanks for reading! Let me know if you have any questions and have a great week.

Pat

This is not investment advice. The opinions expressed and the information contained herein are based on sources believed to be reliable, but accuracy or appropriateness is not guaranteed. Past performance is interesting but is not a guarantee of future results. Investments in bonds are subject to gains/losses based on the level of interest rates, market conditions and credit quality of the issuer. Indices are not available for direct investment, although in some cases, there may be ETFs available designed to track some of the indices shown. The author does not provide investment, tax, legal or accounting advice. Investors should consult with their own advisor and fully understand their own situation when considering changes to their strategy, tactics or individual investments. Additional information available upon request.

This is not investment advice. The opinions expressed and the information contained herein are based on sources believed to be reliable, but accuracy or appropriateness is not guaranteed. Past performance is interesting but is not a guarantee of future results. Investments in bonds are subject to gains/losses based on the level of interest rates, market conditions and credit quality of the issuer. Indices are not available for direct investment, although in some cases, there may be ETFs available designed to track some of the indices shown. The author does not provide investment, tax, legal or accounting advice. Investors should consult with their own advisor and fully understand their own situation when considering changes to their strategy, tactics or individual investments. Additional information available upon request.

©2016 Patrick F. Luby

All Rights Reserved