Muni Catchup 9/26

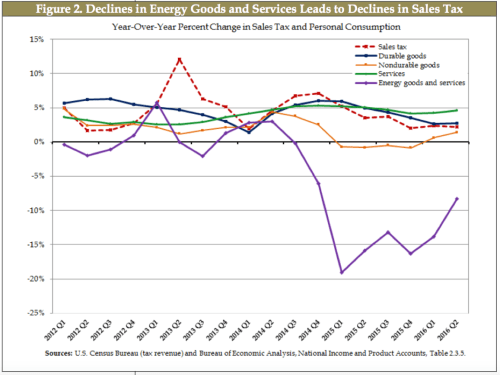

State Tax Revenues Decline

A new report on state tax revenues from The Nelson A. Rockefeller Institute of Government should raise credit concerns for muni bond investors.

State and local government taxes have continued a slowdown that began in the middle of 2015 and that has extended into the second quarter of 2016. State and local government revenue from major taxes tracked by the Census Bureau grew by 3.0 percent in the first quarter of 2016, the most recent quarter for which we have full details, which is a substantial slowing from the 5.4 percent average for the four previous quarters.

Total state tax revenue from all sources grew by 1.6 percent in the first quarter and preliminary data for the second quarter of 2016 indicate declines of 2.1 percent. The declines in state government tax revenues in the second quarter appear to have been driven by the weak stock market of 2015, and by slowing growth in sales tax and withholding collections.

The outlook for state budgets in the 2016-17 state fiscal year, which began on July 1st in forty-six states, remains gloomy.

State Revenue Report, September 2016.

Even though most local governments earn the bulk of their tax revenue from property taxes, state tax revenues are important both as an indicator of economic conditions and because of the dependence of so many local governments on state revenue sharing.

While these trends may not be a reason to take immediate action, they do bear watching–particularly for self-directed investors with exposure to issuers with a narrow margin of financial safety.

Have You Been Waiting on The Fed?

Hurry up and wait! Well, according to new data, muni investors have not been waiting on the Fed. In fact, individual investors have been adding exposure to munis. In case you missed it, please see my article on ETF.com or the special Catchup from 9/16.

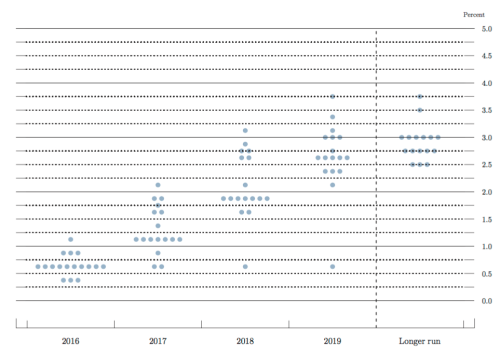

The Dot Plot

Fed watchers were anxiously awaiting the pronouncement from last week’s FOMC meeting…in case you missed my comments, see my special Catchup 9/21.

The Bottom Line

Curve: Continue with a cautious stance as it pertains to maturity selection. Going out to 10-years picks up almost half of the available yield in the curve (see the Context page for details), but with much less risk. You don’t have to draw an artificial line in the sand right at ten years, but understand the duration risk of going longer out the curve.

Credit: It’s never a good idea to overload on any one source of risk, and credit risk gone bad can be especially painful to exit, but holding a modest amount of credit risk is reasonable given the current environment, and can add some incremental income as well as diversification. If you’re holding or are thinking about adding non-investment grade bonds, consider hiring a professional manager–either through an SMA, mutual fund or an ETF. (You saw my note above about the Rockefeller report, right?) Credit risk is often more correlated with equity risk than interest rate risk is, so overweighting your fixed income with credit risk may be reducing overall portfolio diversification. Be careful, and seek expert guidance if you need it.

Structure: Premium bonds remain favored for their lower duration and higher cash flow.

Calls: Don’t give away your call protection for free! Rates could go lower, so beware of the total call risk in your portfolio. There are attractive opportunities right now for short call “kicker” bonds that would have higher yields to maturity if they don’t get called–but be sure that you are well compensated for that extension risk. If you are going to accept call risk, be sure that you are getting paid to do so.

Products: muni bond mutual funds continue to have huge inflows. (Muni ETF flows have also been positive, but the dollar amounts are much less. See the Context page for recent data.) If those flows stop, that could take a lot of demand pressure out of the market, further pressuring muni prices, and if the flows reverse, even investors who remain in those funds could get hurt by fellow shareholders heading for the exits. For right now, though, the addition of two new muni bond ETFs from Van Eck is a good sign of demand and support for the market.

Have a great week, and thanks for reading. Please let me know if you have any questions.

Pat

If you really want to accurately forecast rates, read my

If you really want to accurately forecast rates, read my

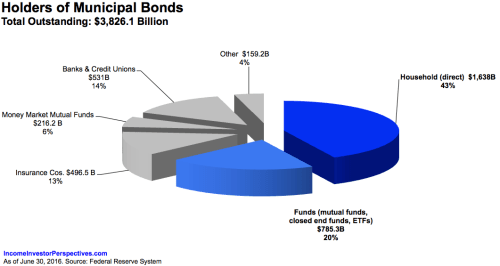

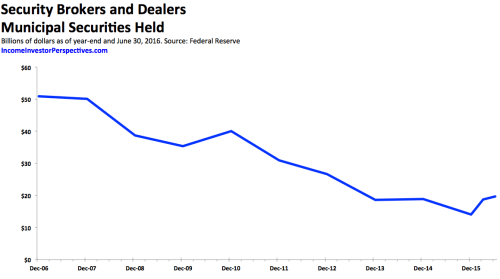

Source: Federal Reserve, September 16, 2016. Dollar amounts in billions.

Source: Federal Reserve, September 16, 2016. Dollar amounts in billions.

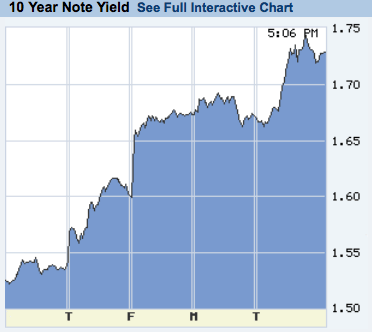

It was a painful day in the bond market (5-day chart of the U.S. Treasury 10-year note is below), so I’m just posting this in case you missed my article yesterday on Seeking Alpha, because it’s even more relevant now than it was yesterday.

It was a painful day in the bond market (5-day chart of the U.S. Treasury 10-year note is below), so I’m just posting this in case you missed my article yesterday on Seeking Alpha, because it’s even more relevant now than it was yesterday.