Muni Catchup 6/13

Welcome to Pat Luby’s Muni Catchup for June 13, 2016

The FOMC meets this week, so in anticipation of that, I decided to update one of my favorite charts–even though it will be out of date by Thursday. The chart below shows a forecast for the Fed Funds Target Rate based on the most recent FOMC Dot Plot, a new version of which is expected after this week’s meeting. The visual here is striking, and I show it in case anyone out there is not convinced yet that the Fed needs to adjust their timing for rate hikes, because clearly the market and the now out-of-date Dot Plot are saying two different things.

The FOMC meets this week, so in anticipation of that, I decided to update one of my favorite charts–even though it will be out of date by Thursday. The chart below shows a forecast for the Fed Funds Target Rate based on the most recent FOMC Dot Plot, a new version of which is expected after this week’s meeting. The visual here is striking, and I show it in case anyone out there is not convinced yet that the Fed needs to adjust their timing for rate hikes, because clearly the market and the now out-of-date Dot Plot are saying two different things.

Looking at this online–or worse, on your phone–will make you go blind. Click here to open a legal size PDF version of this chart.

The prospect of rising rates is a two-edged sword–of course bond market investors are anxious for higher yields and cash flows, but are concerned about the potential decline in value of their existing holdings. When the Fed does begin to raise rates, it will be because of signs of economic growth. When that happens, other bond market relationships should also be expected to change–such as tightening credit spreads and flattening yield curve, both of which could mitigate potential declines in market values (or NAVs for fund holders). Investors who reinvest their cash flow would benefit almost immediately from higher earnings on their interest payments. (Which is why so many institutional portfolio managers prefer higher coupon bonds–in order to have more cash flow available to reinvest at higher future rates.) Finally–since it has been many years since most bond investors have tweaked their portfolios by using tax-loss swaps, it would be prudent to refresh yourself in the next couple of months about how they work and how to avoid the wash sale rule, so that after Labor Day–if rates are higher, you won’t be scrambling to decide what to do and how to do it.

Recent Rate Trends

As shown above and the table below, rates continued to (mostly) decline last week.

When compared to U.S. Treasury yields, which obviously benefit from global demand, long muni yields are very attractive. So it is not surprising that last week’s Flow of Funds Report from the Federal Reserve showed that non-U.S. ownership of munis increased by $2 billion in Q1 ’16. Non U.S. investors now hold $89.2 billion in munis. In comparison–muni ETFs–which have been attracting new assets at a speedy clip–held $20.3 billion as of the end of Q1. (If you subscribed you’d have read all of this already, but if you missed it, see the Muni Catchup from 6/10.)

By the way, I have more data about the market on the Muni Market Yields in Context page.

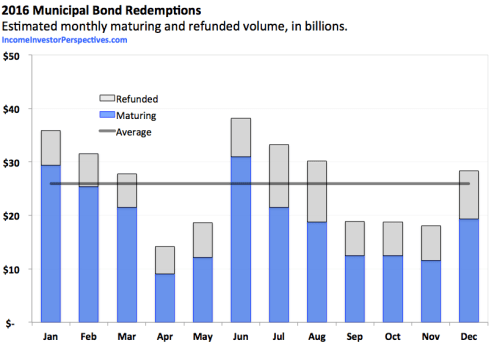

Summer Solstice

Astronomically speaking, summer doesn’t begin until next week–the solstice falls on June 20. But, “Summer Redemption Season,” the three months of heavy muni bond redemption activity–started June 1st, and continues through July and August. (I’ve updated the article with estimated July redemption amounts for key states.)

If you have bonds maturing or getting called away, don’t let the returned principal sit around doing nothing until after Labor Day. Plan ahead.

The next regular Muni Catchup is scheduled for Monday, June 20. Since the FOMC is meeting this week, there’s a good chance that there will be an interim update.

The next regular Muni Catchup is scheduled for Monday, June 20. Since the FOMC is meeting this week, there’s a good chance that there will be an interim update.

If you are not already subscribed, be sure to sign up to be notified by email when new items get published.

If you find this to be helpful, please let me know. Your comments and questions are welcome and appreciated.

Thanks for reading,

Pat

The opinions expressed and the information contained herein are based on sources believed to be reliable, but accuracy or appropriateness is not guaranteed. Past performance is interesting but is not a guarantee of future results. Investments in bonds are subject to gains/losses based on the level of interest rates, market conditions and credit quality of the issuer. Indices are not available for direct investment, although in some cases, there may be ETFs available designed to track some of the indices shown. The author does not provide investment, tax, legal or accounting advice–this is not investment advice. Investors should consult with their own advisor and fully understand their own situation when considering changes to their strategy, tactics or individual investments. Additional information available upon request.

©2016 Patrick F. Luby

All Rights Reserved

The opinions expressed and the information contained herein are based on sources believed to be reliable, but accuracy or appropriateness is not guaranteed. Past performance is interesting but is not a guarantee of future results. Investments in bonds are subject to gains/losses based on the level of interest rates, market conditions and credit quality of the issuer. Indices are not available for direct investment, although in some cases, there may be ETFs available designed to track some of the indices shown. The author does not provide investment, tax, legal or accounting advice–this is NOT investment advice. Investors should consult with their own advisor and fully understand their own situation when considering changes to their strategy, tactics or individual investments. Additional information available upon request.

The opinions expressed and the information contained herein are based on sources believed to be reliable, but accuracy or appropriateness is not guaranteed. Past performance is interesting but is not a guarantee of future results. Investments in bonds are subject to gains/losses based on the level of interest rates, market conditions and credit quality of the issuer. Indices are not available for direct investment, although in some cases, there may be ETFs available designed to track some of the indices shown. The author does not provide investment, tax, legal or accounting advice–this is NOT investment advice. Investors should consult with their own advisor and fully understand their own situation when considering changes to their strategy, tactics or individual investments. Additional information available upon request.