Muni Catchup 5/31

by PL

Welcome to Pat Luby’s Muni Catchup!

Ingredients:

- Comments

- Context

- Performance

- Flows

- Notes

Comments

The markets appear to be adjusting to the idea of a Fed rate hike. In the bond markets, while the shorter end of the yield curves have moved slightly higher in yield–the muni curve has moved by less than the Treasury curve, though that is not surprising given the large amounts of new money flowing into the muni market (see Flows, below). With over $100 billion in muni money maturing over the next three months, demand is likely to remain strong, although once the Summer Redemption Season passes, the balance of supply and demand may tilt toward lower prices and (slightly) higher yields. But that is a long way off, and I have never been a fan of trying to forecast rates. (If you haven’t already read my article about Timing Interest Rates, please go read it right now. Come back here when you are done.)

For advisors or investors with matured muni principal to put back to work, if you find it difficult to immediately replace your old bonds with something of comparable quality and characteristics, you can consider using muni ETFs as a placeholder for your muni exposure. I have written a guide to How to Pick the Right Muni ETF. (Of course my subscribers cannot claim that they did not have ample opportunity to provide for reinvestment of their maturing bonds, as I have been writing about Summer Redemption Season for several months.)

Context

Even though most individual investors are (or should be) goal oriented, it is prudent to pay attention to what is going on in the broader bond market. The weekly Context section of my Catchup provides a brief overview of munis versus U.S. Treasury benchmarks. Wondering which maturity to invest in? First of all it will depend on your goal, but if you are open-minded about where to be on the curve, it is helpful to look at the “Percent of Max Yield” in combination with the Modified Duration–you can get a sense of how much of the maximum available yield you can get in comparison to the relative amount of interest rate risk (Duration) you would be taking. Read this article to learn more about the Duration calculation and how to use it.

I suggest that you print out the Context page and keep it by your phone and computer for the week. It is suitable for hanging or wrapping fish. (When I was growing up, every issue of Mad Magazine included an advertisement to order your own copy of the portrait of their famous (and fictitious) “mascot,” Alfred E. Neuman, whose portrait was emblazoned with the question, “What~~Me Worry?” You may recall that those ads encouraged you to order multiple copies, as they were also suitable for hanging or wrapping fish. “What~~Me Worry?” may be a humorous slogan for a fictitious character, but it is not an appropriate approach to managing your investments. While you may be properly positioned, paying attention to the context of what is going on around you and your investments is always a good idea because market psychology can change so quickly. Hence, I always lead with the Context.

Performance

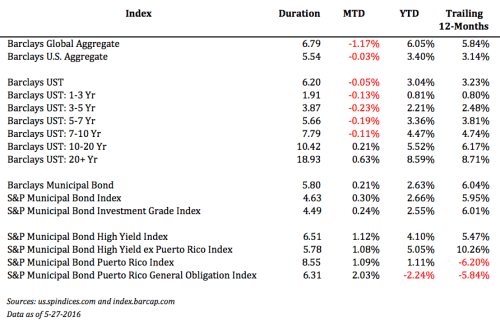

Duration has been the bond investors’ friend…is that beginning to change? And, are prices on Puerto Rico munis ready to turn the corner?

First, let’s look at Duration. Using the Barclays UST indices as a tool to strip out the credit risk, notice how the Trailing 12-Months returns go up as the Duration goes up, while Month-to-Date returns are mostly negative. It’s interesting to note, though, is that the two longest Duration indices are positive.

With the FOMC now widely expected to hike the Fed Funds rate at their meeting on June 14 & 15, shouldn’t all rates be moving higher? Well no, not necessarily. Because the Fed Funds rate is an overnight lending rate, it has the greatest influence on the short end of the yield curve. Since long-term investors know that the Fed Funds rate will fluctuate over the holding period of a long-term bond, longer-duration rates tend to react more to inflation expectations than to fluctuations in the Fed Funds rate. So while short-maturity yields have moved higher in May, long Treasury yields are back to about where they were at the start of the month. (See the Context page for additional data.)

Are the prices on Puerto Rico bonds ready to turn the corner? Note that the two S&P Puerto Rico indices above have positive performance for the Month-to-Date–indicating recently improving prices. While there is MUCH uncertainty that remains for these bonds, the prospect of a bipartisan Federal legislative plan seems to be providing confidence for some speculators to get more active in the last couple of trading sessions. While some Puerto Rico bond prices may have improved lately, they are still speculative investments–it would be premature to expect that prices are ready to turn the corner and head higher. The legislation has not been signed into law, and there are large June 1st payments due. For investors in funds and ETFs with P.R. exposure, you may see improved NAVs as a result of the recent improvement in prices.

NOTE: The indices above are Total Return Indices. Each index is calculated based on the change in price of the underlying baskets of bonds, plus the amount of interest earned in the period. A decline in the price of the basket could still result in a positive Total Return if the amount of interest earned exceeds the price decline. An improving trend (that is, higher rates of return for more recent periods) indicates improving prices for the sector represented by the index. The reverse is also true–a declining trend, in which past returns are higher than recent returns, suggests that the market is expecting diminishing future performance.

Flows

Based on net flows into muni bond mutual funds and ETFs, demand for professionally managed muni bonds remains very strong. With Summer Redemption Season kicking off in June, a meaningful amount of the $38 billion in maturing June principal may find its way into mutual funds and ETFs, so I would not be surprised to see an additional uptick in net fund in-flows during the weeks ahead.

Dollar amounts are in millions. Source: Investment Company Institute, May 25, 2016.

Notes

I added a new link to my Links of Note page. Have you checked out my list? Let me know what you think.

Because some weeks will need to have more than one serving of Muni Catchup, each Catchup will now arrive with the date in the headline to help you be sure that you are up to date.

The next Muni Catchup is scheduled for Monday, June 6, but there will be additional updates this week, so if you are not already subscribed, be sure to sign up to be notified by email when they are published.

Comments and questions are welcome and appreciated.

Have a great week,

Pat

The opinions expressed and the information contained herein are based on sources believed to be reliable, but accuracy or appropriateness is not guaranteed. Past performance is interesting but is not a guarantee of future results. Investments in bonds are subject to gains/losses based on the level of interest rates, market conditions and credit quality of the issuer. Indices are not available for direct investment, although in some cases, there may be ETFs available designed to track some of the indices shown. The author does not provide investment, tax, legal or accounting advice–this is NOT investment advice. Investors should consult with their own advisor and fully understand their own situation when considering changes to their strategy, tactics or individual investments. Additional information available upon request.

[…] In the red for the month–as with Treasuries–was the intermediate portion of the muni yield curve, where yields have been ticking higher as the market adjusts to the increasing likelihood of a June rate hike by the Fed. As I wrote for yesterday’s Catchup: […]

LikeLike