Muni Catchup Summer Solstice Edition

by PL

June 20: The First Day of Summer in the Northern Hemisphere

Welcome to the Muni Catchup! It’s now official–today is the first day of summer. Around here, it has felt like summer for several weeks. In past years, markets got slower and quieter in the summer, but not anymore–and this week is not going to be a quiet or slow week.

Welcome to the Muni Catchup! It’s now official–today is the first day of summer. Around here, it has felt like summer for several weeks. In past years, markets got slower and quieter in the summer, but not anymore–and this week is not going to be a quiet or slow week.

Munis & Brexit

Brexit (the UK referendum on whether the country should remain in the European Union) is going to be all over the news this week and has the potential to send ripples across all the markets around the world…even the muni bond market.

Perhaps not as much because of the immediate market reaction (which could affect currency and bond markets), but because of the long-term implications.

I write not as an economist, but as a student of the markets and an interested observer of the economy. Should the UK leave the EU, it would reduce the likelihood of the Euro ultimately achieving equal status with the dollar as a reserve currency, and it is the exclusive status as the world’s currency that has allowed many of the U.S. fiscal and monetary policies that–in my view–have added friction to the economy and reduced growth, with obvious implications for the bond markets and interest rates.

If the UK exits the EU, that could be bullish for the U.S. dollar, and push our interest rates lower–as we have seen over just the last two weeks. Some of this seems to be already priced into the markets…but is there more? What happens if the vote is to stay in? Will some of the recent rally unwind? Currency markets are large and liquid, and when money moves to a “safe haven,” it is often put into the bond markets–that is why muni bond investors should be paying attention to the Brexit vote. Investors have been waiting for years for yields to “go back up,” but there are forces that could actually push yields lower.

The vote is Thursday, with the results likely to be announced early Friday in London–making for a fascinating check on the markets when we all wake up Friday morning.

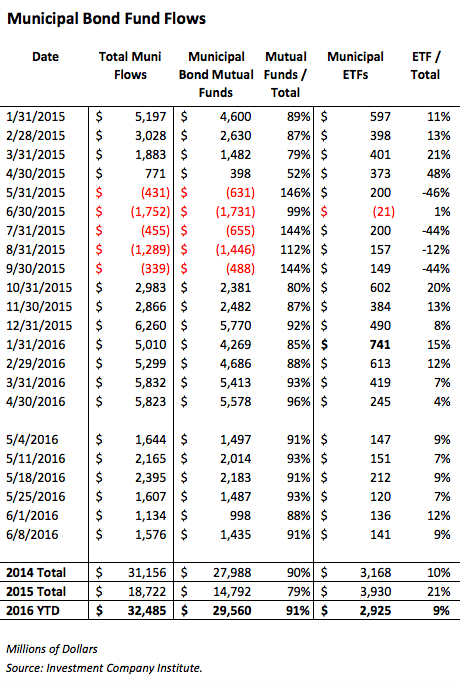

Muni Bond Market Yield Opportunities

Rates keep going down, and investors keep putting money into munis (see the Flows table, below). Since I wrote about the surprising first quarter muni buying from non-U.S. investors, several other commentators have written about the same topic. It is not surprising when you look at global rates (click here to go to Bloomberg.com’s global rates page), U.S. rates and muni rates in particular look attractive. See my weekly Muni Yields in Context page for additional data on the muni market.

If you are looking for specific ideas in the muni ETF market, see my article posted today on ETF.com, Yield Opportunities Abound in Muni ETFs.

Wondering if you should wait to put money to work or wait until after the vote? There are so many forces that affect the markets and interest rates that forecasting them is (nearly) impossible. When professional portfolio managers come in the morning, if there is new money to put to work, they don’t decide whether or not they will invest that money, they decide where to invest that money. That has been and remains my opinion–don’t let money sit around doing nothing–put it to work. Letting your money retire will only delay your own retirement. If you still want to try to time rates, then read my primer on How to Time Interest Rates. For the rest of you, if your investment plan indicates that you need fixed income, consider going out far enough to at least equal the rate of inflation to retain purchasing power. With the potential for rates to be pressured lower, if you are going out the curve, it may be worth paying up a little for additional call protection.

Don’t forget about Money Market Fund Reform!

As I noted in the Muni Catchup 6/10, money market mutual fund holdings of munis dropped by $29.3 billion in Q1, even as total money market mutual fund assets in the quarter increased by $4.1 billion. (Holdings of U.S. Treasury securities increased by $62.6 billion.) Keep in mind portfolio managers are preparing for the October deadline for implementing a floating NAV on institutional money market funds. There may be a continued shift of holdings in some money market funds from municipals into more-liquid U.S. Treasury securities. If you need a refresher on the reform, the ICI has a nice summary available here.

The next regular Muni Catchup is scheduled for Monday, June 27. But I recommend that if you are not already signed up for the e-mail updates, do it now. There are some special reports in the pipeline, and you won’t want to miss them.

Your comments and questions are welcome and appreciated. What do you like about the Muni Catchup? What would make it more helpful for you? Let me know!

Thanks for reading,

Pat

The opinions expressed and the information contained herein are based on sources believed to be reliable, but accuracy or appropriateness is not guaranteed. Past performance is interesting but is not a guarantee of future results. Investments in bonds are subject to gains/losses based on the level of interest rates, market conditions and credit quality of the issuer. Indices are not available for direct investment, although in some cases, there may be ETFs available designed to track some of the indices shown. The author does not provide investment, tax, legal or accounting advice–this is not investment advice. Investors should consult with their own advisor and fully understand their own situation when considering changes to their strategy, tactics or individual investments. Additional information available upon request.

©2016 Patrick F. Luby

All Rights Reserved

[…] Are you sick of hearing about it already? You can’t say I didn’t warn you! Here’s what I wrote in last week’s Catchup: […]

LikeLike