Muni Bond DIFM is Growing

Muni Bond DIFM Ownership is Growing

Muni Bond DIFM Ownership is Growing

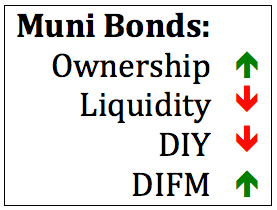

Rates are low and the Fed is on hold; municipal finances are stressed and bond market liquidity is down. While there would seem to be lots of reasons for investors to be avoiding municipal bonds, individual investors were actually net buyers of municipal bonds last year—but not through the traditional means of adding individual bonds to their portfolios.

Last year, according to data from the Federal Reserve, fewer individual investors were opting for the DIY (“Do It Yourself”) model of managing individual bonds on their own, and there was growth in the use of professionally managed (“Do It For Me,” or DIFM) mutual funds and ETFs.

Data from the Federal Reserve show that direct individual investor ownership of municipal bonds declined by over $25 billion last year, however, indirect ownership through muni bond mutual funds and ETFs grew significantly.

|

2014 |

2015 |

Change |

||

|

Total Outstanding |

$3,652.4B | $3,714.8B | +$62.4B | +2% |

| Households (direct) |

$1,540.4B |

$1,514.8B |

-$25.6B |

-2% |

|

Mutual Funds |

$657.7B |

$705.4B |

+$47.7B |

+7% |

|

ETFs |

$14.6B |

$18.5B |

+$3.9B |

+27% |

The positive flows into mutual funds and ETFs are continuing this year. Through March 9, muni bond mutual funds have attracted $10.7 billion in new assets (according to the Investment Company Institute) and muni ETFs have added almost $1.5 billion (according to FactSet data).

Part of what may be driving the shift away from DIY into DIFM…..

Click HERE to continue reading the complete article on ETF.com