Muni Catchup 10/10

by PL

This week in The Muni Catchup:

This week in The Muni Catchup:

- Seeing Red

- Duration is No Longer Your Friend

- Market & Calendar Preview

- Market Wisdom

- Money Market Fund Assets & Flows

- The Bottom Line

Seeing Red

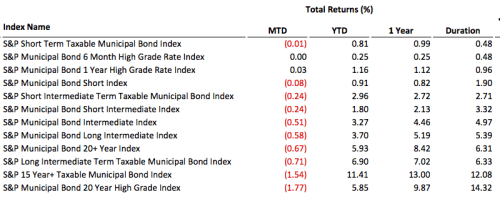

Take a look at the recent month-by-month total returns for the muni market and you’ll see that even though the YTD returns are positive, the recent trend suggests a change in momentum.

As shown in the table below, duration is no longer your friend. When the bond markets are rallying (prices rising/yields declining), more duration often can mean more return, but when the market shifts, more duration can mean more downside risk. With the end of the week sell-off in bonds, the performance of the S&P Dow Jones muni indices revealed the impact of higher duration. (The list below is sorted in duration order.)

By the way, I’m assuming that you have already looked at and printed out this week’s Context page. If you haven’t, please go do that now.

Preview

Even with the 4-day week in the bond market, new issue muni supply remains robust, with $8.4 billion scheduled for the week. The U.S. Treasury will be auctioning 3, 10 and 30-year debt this week, so the Treasury market is likely to remain soft in advance of that new supply coming into the market. However, keep in mind that bond fund flows remain positive, so if there is strong enough demand to absorb this week’s heavy muni and Treasury supply, don’t be surprised if yields finish the week lower.

Important Dates

| 10/10 Monday | Columbus Day | stocks open / bonds closed |

| 10/12 Wednesday | Yom Kippur | |

| 10/14 Friday | effective date for Money Market Fund reform | |

| 11/1 & 2 Tue & Wed | FOMC meets | |

| 11/2 & 3 Wed & Thu | Inside ETFs: Inside Fixed Income 2016 | |

| 11/8 Tuesday | Election Day | |

| 11/11 Friday | Veterans Day | stocks open / bonds closed |

| 11/24 Thursday | Thanksgiving Day | all U.S. markets closed |

| 12/13 & 14 Tue & Wed | FOMC meets | |

| 12/25 Sunday | Christmas Day | |

| 12/25 Sunday | Chanakuh begins | |

| 12/26 Monday | Christmas Observed | all U.S. markets closed |

| 12/30 Friday | Last Trade Date of the year | bonds close early |

Here’s a link to the complete economic calendar on the MSRB’s EMMA website.

Market Wisdom

Targeting arbitrary hurdles quickly leads to undisciplined and, in the end, unproductive, investment management.

From Due Diligence, by Christopher Carosa.

This quote points out the importance of planning as the necessary prerequisite to investing. None of us can control the market or the returns available, but we can control our asset allocation, investment selection and costs. Yes, it is important to watch the benchmarks to follow the market, but it is also important to have a plan (or investment policy) and to stick with it.

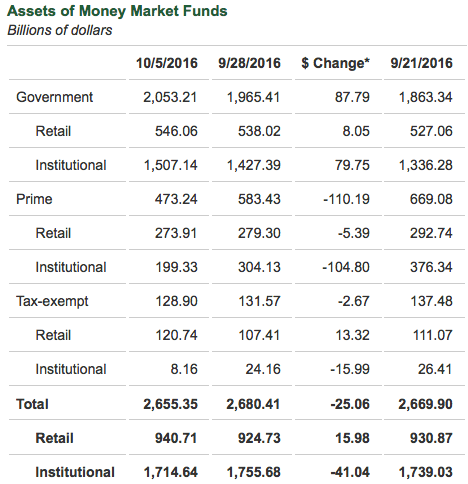

Money Market Funds Update

Tax-exempt money market funds declined by $2.6 billion last week, but the big number there is the continued dramatic decline in the assets for institutional tax-exempt money market funds. If you missed it, see last week’s Catchup for more background on money market fund reform.

Source: ICI

The Bottom Line

Shortened week and heavy supply may present some buying opportunities for investors.

Curve: Continue with the cautious stance as it pertains to maturity selection. For investors with new money to put to work or reinvest, favoring the shorter end of your maturity (or duration) target range can make sense.

Credit: Holding a modest amount of credit risk can add some incremental income as well as diversification. If the economy continues to improve and pushes rates higher, that should also tighten credit spreads, which could offset some of the duration risk. But as always, if you’re thinking about adding non-investment grade bonds, consider hiring a professional manager–either through an SMA, mutual fund or an ETF.

Structure: Premium bonds remain favored for their lower duration and higher cash flow. Some pre-refunded bonds have been offered at more than 100% of Treasury yields recently, making the yields attractive for “pre-re” buyers.

Calls: Beware of the total call risk in portfolios. There are attractive opportunities right now for short call “kicker” bonds that would have higher yields to maturity if they don’t get called–but be sure that you are well compensated for that extension risk. If you are going to accept call risk, be sure that you are getting paid to do so.

Products: Muni bond mutual fund and ETF inflows continue to be positive. Favor lower duration solutions.

Sellers: Investors who will be selling should pay attention to the calendar and the overall tone of the bond markets–watch the 10-year U.S. Treasury for direction. If the Treasury auctions do well, look for a better bid-side to the market later in the week.

Have a great week, and thanks for reading. Please let me know if you have any questions.

Pat

This is not investment advice. The opinions expressed and the information contained herein are based on sources believed to be reliable, but accuracy or appropriateness is not guaranteed and are subject to change without notice. Past performance is interesting but is not a guarantee of future results. Investments in bonds are subject to gains/losses based on the level of interest rates, market conditions and credit quality of the issuer. Indices are not available for direct investment, although in some cases, there may be ETFs available designed to track some of the indices shown. The author does not provide investment, tax, legal or accounting advice. Investors should consult with their own advisor and fully understand their own situation when considering changes to their strategy, tactics or individual investments. Additional information available upon request.

©2016 Patrick F. Luby

All Rights Reserved