Muni Catchup: T.S. Eliot Was Wrong

by PL

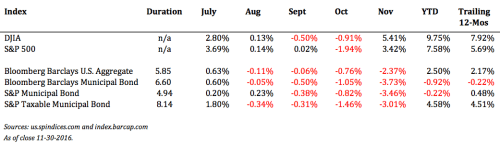

T.S. Eliot was wrong…November is the cruelest month. (At least it was this year.) Fixed income total return indices turned in the worst performance in a long time. Duration is no longer the investor’s friend.

T.S. Eliot was wrong…November is the cruelest month. (At least it was this year.) Fixed income total return indices turned in the worst performance in a long time. Duration is no longer the investor’s friend.

- But has the bond market sold off too much?

- Are rates going to continue to go higher?

- Or, could they go lower from here?

- What happens if the various votes in Europe put pressure on the Euro? Will assets flow into U.S. Treasuries? What if the votes strengthen the position of the Euro?

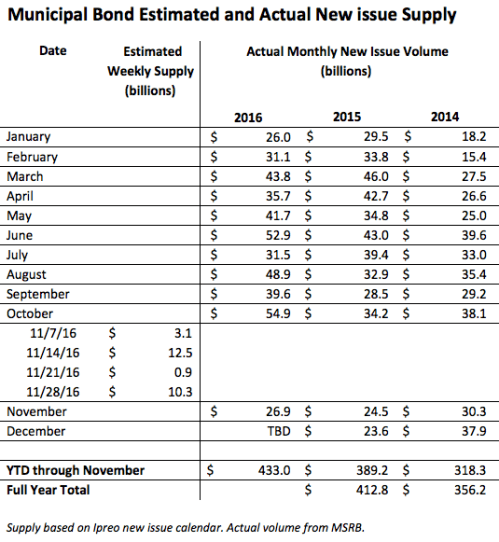

- How about munis? Mutual funds are losing assets while issuance remains heavy. Are munis going to cheapen further? How might tax reform affect yield ratios?

Clearly, much uncertainty continues to swirl around the markets.

The emotional reaction to the market turmoil might be to exit fixed income. But what would Ben Graham would do? I would expect that he would remind investors that the chances for long-term success are improved when emotion is eliminated from the investment decision-making process–decisions should be based on arithmetic not optimism (or fear). We encourage investors to take that advice to heart and to maintain their appropriate asset class exposure as determined by their plan, because no matter what you think is going to happen, it is possible that the opposite will happen. However, for those portfolios that are overweight duration, it is prudent to consider scaling it back. Using low duration fixed income ETFs can be one way to quickly do that.

Finally, in order to help reduce the risk of April being the cruelest month, use the remaining weeks of the year to harvest losses–especially from long-duration fixed income positions. Tax-loss swaps can be a helpful tool when seeking to adjust the portfolio duration.

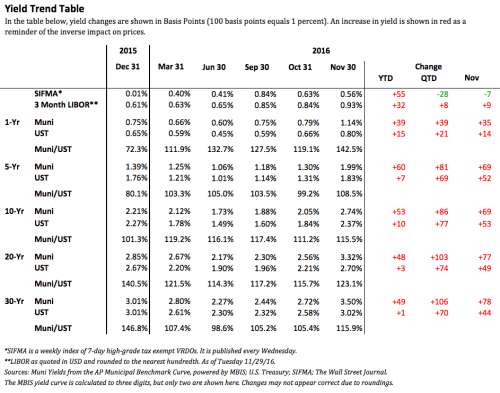

We are now using the AP Municipal Benchmark Curve, Powered by MBIS as our indicator of municipal market yields. The Associated Press (AP) – Municipal Bond Information Service (MBIS) U.S. Tax-Exempt Municipal Index covers the long-term tax-exempt municipal bond market and is based on actual trades and market quotes in the municipal bond market. The curve tracks the offered side of the market and includes smaller transaction sizes to reflect what individual investors may see in the market. The curve assumes 5% coupons with 10 year call protection. The curve is available to subscribers at http://www.mbis.com/apindex/ and is also distributed by The Associated Press to newspapers around the country.

Thanks For Reading

Pat

This is not investment advice. The opinions expressed and the information contained herein are based on sources believed to be reliable, but accuracy or appropriateness is not guaranteed and are subject to change without notice. Past performance is interesting but is not a guarantee of future results. Investments in bonds are subject to gains/losses based on the level of interest rates, market conditions and credit quality of the issuer. Indices are not available for direct investment, although in some cases, there may be ETFs available designed to track some of the indices shown. The author does not provide investment, tax, legal or accounting advice. Investors should consult with their own advisor and fully understand their own situation when considering changes to their strategy, tactics or individual investments. Additional information available upon request.

©2016 Patrick F. Luby

All Rights Reserved

[…] T.S. Eliot was wrong? If not, that means that you missed the November market recap. Here’s the link to it so you can go read it […]

LikeLike