Muni Catchup 12-8

by PL

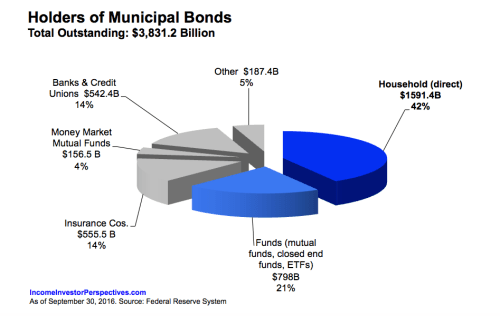

Muni Holders: Timing is Everything

The latest data about muni bond ownership came out today, and in an example of unfortunate timing, in the third quarter (right before the recent increase in rates), individual investors reduced their direct ownership of munis by $6.5 billion, but increased indirect ownership though mutual funds by $13.5 billion. While individual bonds do go down in value when interest rates go up, because mutual funds are managed to maintain duration, it can take much longer for their NAVs to recover from a decline.

Other notable Q3 changes in municipal ownership:

- Non-U.S. investors increased their holdings by $3.6 billion. (Not surprising given the negative interest rate world outside of the U.S.)

- Insurance companies increased their holdings. Property and Casualty companies by $3.4 billion and Life companies by $1.8 billion.

- ETFs increased by $1.4 billion. (But regular Catchup readers know that already.)

- Non-muni bond mutual funds hold $17.0 in munis, a decline of $1.6 billion in the quarter, but still a significant increase from the $10.3 billion held at year-end 2015.

- Bank ownership increased by $11.5 billion.

- Money Market Mutual Fund holdings dropped by $57.4 billion. (This is not surprising, given the recent reform in Money Market Mutual Fund regulations.)

See next week’s Muni Catchup for more data and analysis on today’s numbers.

If you do not already subscribe to receive The Muni Catchup via e-mail, you should do so right now. The subscription form is below. As a reminder, there is no charge for The Muni Catchup, but if you find it helpful, you can help by sharing it.

The Muni Catchup is not investment advice. The opinions expressed and the information contained herein are based on sources believed to be reliable, but accuracy or appropriateness is not guaranteed and are subject to change without notice. Past performance is interesting but is not a guarantee of future results. Investments in bonds are subject to gains/losses based on the level of interest rates, market conditions and credit quality of the issuer. Indices are not available for direct investment, although in some cases, there may be ETFs available designed to track some of the indices shown. The author does not provide investment, tax, legal or accounting advice. Investors should consult with their own advisor and fully understand their own situation when considering changes to their strategy, tactics or individual investments. Additional information available upon request.

©2016 Patrick F. Luby

All Rights Reserved