Muni Catchup 11/28

This Week in the Muni Catchup:

This Week in the Muni Catchup:

- Rates Continue to Backup–will they attract buyers?

- The Tide Has Turned–will the heavy outflows from bond funds continue?

- Did You Read About Dallas? Has a new fault line emerged in the muni market?

- Supply–will new issue muni supply increase under President Trump?

- The Bottom Line

Self-directed investors are putting themselves at risk if they are not doing their homework and surveilling the credits in their portfolio.

From “A New Fault Line in the Muni Market?,” below.

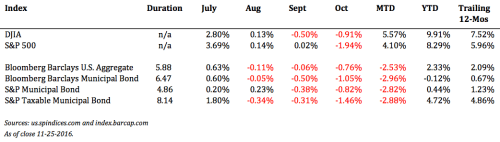

Rates Continue to Backup

Most bond market yields are now higher on the year–a good thing for investors who have been waiting on higher rates and more income, but a painful turn of events for investors in mutual funds who will be seeing declines in their NAVs. Is it time to capitulate and sell? Or, is it time to buy? One answer does not fit all, but the answer does depend on your time horizon–for investors, the answer is different from traders.

This week and the following two weeks will be good indicators of what the new trading ranges will be–there are no holidays or elections to distract market participants, so with more normalized volume, it will be interesting to see where the market finds equilibrium. The week after the election, trading volume was unusually heavy–average daily par amount traded was 27% above the current seasonal* (post-Labor Day) average while last week, volume was unusually light–26% below the seasonal average.

*For an explanation of how we look at the seasons in the muni market, please read “Three Seasons” in The Muni Catchup 9/6.

The Tide Has Turned

Municipal bond mutual fund flows have reversed–dramatically.

Municipal bond market participants were not surprised when Lipper reported that for the week ended November 16 municipal bond mutual funds lost an estimated $2.8 billion in assets. On Friday, they followed up by reporting their estimate that for the week ended the 23rd muni funds lost an additional $2.2 billion. Meanwhile, ICI, whose data are more complete but lags Lipper by a week, reported that for the week ended the 16th, muni funds lost $4.5 billion. Because of the differences in methodology, it is difficult to compare the two sets of data, but clearly the long trend of inflows to muni bond funds has changed.

If this year’s huge inflows were primarily from long-term investors, it would be surprising to see the current pace of outflows to continue. If, however, assets were put into munis as a short-term “parking” spot, then flows will continue–particularly if the equity market continues to do well.

A New Fault Line in the Muni Market?

Is a new fault line opening up under the municipal bond market? Because of the long history of creditworthiness among investment grade municipal bond issuers, non-professional individual investors have been very comfortable owning municipal bonds…in fact, they dominate the market. But some of the recent headlines should serve as a wake-up call for “buy and hold” investors. The growth in pension-related risk should be of growing concern to investors. In our view, not because of a significant increase in default risk–which does not appear to be imminent–but to a potential increase in liquidity risk.

Because investors rely on the promise of borrowers to pay, a reduction in the ability to pay will be priced into the market. With the decline in overall market liquidity, the increase in perceived credit risk may mean wider bid/ask spreads or even fewer interested bidders when it comes time to sell.

The credit stresses in the muni market are not isolated. Here are some helpful insights from Tom Kozlik at PNC:

I now estimate that approximately 20% of state and local governments are experiencing some type of notable credit deterioration or are currently structurally imbalanced.

[H]ardly anyone…recognize[s] the U.S. state and local government bond market has branched into two distinct segments.

An Evolution in Thinking About Municipal Credit by Tom Kozlik, PNC Capital Markets Municipal Strategist

A practical (and current) example can be found in Dallas, as detailed in two recent articles:

- WSJ, Dallas Police and Fire Pension Fund Beset by Withdrawals

- NY Times, Dallas Stares Down a Texas-Size Threat of Bankruptcy

If you would like to dig deeper into understanding some of the pension funding risks among cities, states, counties, etc., read An Overview of the Pension/OPEB Landscape by the Center for Retirement Research at Boston College.

What’s the takeaway from all this? Even if there is not a change in default rates, credit stresses are rising, and self-directed investors are putting themselves at risk if they are not doing their homework and surveilling the credits in their portfolio. For investors unprepared or unable to do that, now may be the time to consider professional management via mutual funds, ETFs or SMAs (Separately Managed Accounts).

Please see this classic article for more insights about professional management.

Supply

The new issue supply has picked up again, and issuers and underwriters will seek to take advantage of three full (five-day) weeks in order to wrap up the year.

Of interest has been the recent speculation that President Trump’s policies will lean heavily on munis to fund infrastructure, leading to an increase in supply. Here’s one recent example.

However, the ability to borrow is different from the ability to service debt. We’ll have to wait to see what the new President proposes, but it is not unreasonable to suspect that many of the most needed infrastructure projects will be in the same areas where pension obligations are a growing concern. An issuer struggling with growing pension obligations will have reduced financial flexibility and borrowing capacity–so it is not automatic that infrastructure need will lead to muni borrowing.

The Calendar

| 12/13 & 14 Tue & Wed | FOMC meets | |

| 12/25 Sunday | Christmas Day | |

| 12/25 Sunday | Chanakuh begins | |

| 12/26 Monday | Christmas Observed | all U.S. markets closed |

| 12/30 Friday | Last Trade Date of the year | bonds close early |

| 1/16 Monday | Martin Luther King Holiday | all U.S. markets closed |

| 1/20 Friday at Noon ET | Inauguration of Pres. Trump | |

| 12/5 Sunday | Super Bowl 51 |

Here’s the link to the complete economic calendar on the MSRB’s EMMA website.

The Bottom Line

Barbell? Ladder? Short-duration? Long-duration? Load up on credit risk? Avoid credit risk?

Tax-loss swaps: yields are up, prices are down. Consider realizing losses, especially from long-duration positions. In order to maintain an appropriate asset allocation exposure, consider lower-duration solutions for the buy-side of swaps. It has been almost a generation since muni bond tax-loss swaps have been broadly doable–interested advisors should start looking at portfolios now for potential swaps.

Curve: favor the shorter end of your duration range. It can be tempting right now to go out to 15-years or so where almost 90% of the yield in the curve can be captured–but note that the duration at that spot of the curve is over 12–that will inflict a lot of pain, particularly on NAV based holdings such as funds. For investors with a portfolio overweighted in duration, consider adding very low duration positions to balance long duration holdings. Adding an ETF to an all-bond portfolio can be an effective and quick way to get that done. See my recent article on the topic here.

Credit: the economic numbers suggest an improving economy, but it is premature to “load up” on credit. A modest exposure to credit risk is a good diversifier, however. Exposure to non-investment grade credit risk should be for no more than 10% of the fixed income allocation and should be done using full-time professional management, such as an SMA, mutual fund or ETF.

Structure: continue to favor premium bonds, but be sure to pay attention to portfolio level exposure to call risk and the potential for bonds that are currently priced to the call to get priced to maturity if rates move higher–which would increase duration risk. (Don’t forget that rates could go down from here, so locking in good call protection makes sense–especially if it can be done with minimal give-p in yield.)

Products: fund flows (into mutual funds and ETFs) have slowed dramatically. Do not chase recent performance, but choose funds or SMA strategies based on how the objective fits with the investor’s goals.

We are now using the AP Municipal Benchmark Curve, Powered by MBIS as our indicator of municipal market yields. The Associated Press (AP) – Municipal Bond Information Service (MBIS) U.S. Tax-Exempt Municipal Index covers the long-term tax-exempt municipal bond market and is based on actual trades and market quotes in the municipal bond market. The curve tracks the offered side of the market and includes smaller transaction sizes to reflect what individual investors may see in the market. The curve assumes 5% coupons with 10 year call protection. The curve is available to subscribers at http://www.mbis.com/apindex/ and is also distributed by The Associated Press to newspapers around the country.

Thanks For Reading

Did you notice the new format this week? The Context page has been eliminated. Comments are welcome. If you find this helpful, you can help me by sharing it.

Have a great week,

Pat

This is not investment advice. The opinions expressed and the information contained herein are based on sources believed to be reliable, but accuracy or appropriateness is not guaranteed and are subject to change without notice. Past performance is interesting but is not a guarantee of future results. Investments in bonds are subject to gains/losses based on the level of interest rates, market conditions and credit quality of the issuer. Indices are not available for direct investment, although in some cases, there may be ETFs available designed to track some of the indices shown. The author does not provide investment, tax, legal or accounting advice. Investors should consult with their own advisor and fully understand their own situation when considering changes to their strategy, tactics or individual investments. Additional information available upon request.

©2016 Patrick F. Luby

All Rights Reserved