Muni Catchup 12/19

This Week’s Ingredients:

- Are Bonds Dangerous?

- Looking Ahead

- The Calendar

- Muni Bond Data and Tables

- The Bottom Line

Are Bonds Dangerous?

Are bonds too risky? Should long-term investors be avoiding them?

If investors have been buying bonds for the same reasons that they have been buying equities–in pursuit of capital gains–then perhaps yes, bonds have gotten too risky, as it will be more difficult to capture capital gains in the immediate future. (It is because of the trend toward higher rates and the risks of declines in market values that we have been encouraging investors to favor shorter duration bonds, and we remain firmly of that opinion. We also remain steadfast in our belief that a change in the prevailing market conditions should not lead to a change in asset allocation. With the level of interest rates rising, it may be prudent for some investors to seek lower interest rate risk in their portfolio by reducing duration.)

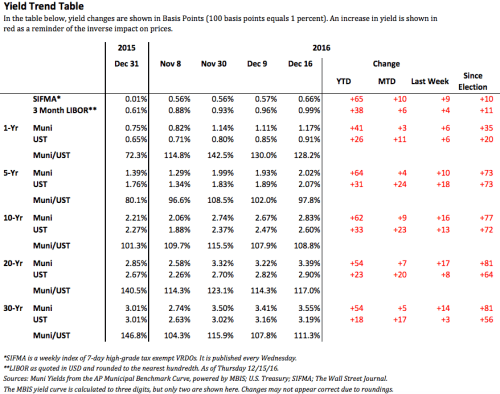

But bonds are not stocks, and most long-term bond investors are interested in the income and diversification that comes with adding bonds to an equity portfolio. It is not surprising, then, that the sharp increase in yields (as shown in our Yield Trend Table, below) has led to an increase in municipal bond trading activity and customer buying. While trading last week was slower than the week before, the pace of activity remains much heavier than the last several months.

Because of the higher yields and cash flows now available in the muni bond market, investors who depend on their portfolios as their primary source of income may be able to reduce their reliance on capital gains or principal withdrawals as funding sources for their cash flow needs.

So no, bonds are not too dangerous. At least not all bonds. Clearly there are risks, but there are also benefits of holding bonds that do not come from holding investments in other asset classes. As we note in The Bottom Line, below, we favor low duration and high cash flow (premium) bonds in order to be able to maintain an appropriate asset allocation with minimal interest rate risk exposure.

Looking Ahead

Since the election, the combination of heavy new issue muni supply and sharply higher muni and Treasury yields have stimulated secondary market trading activity. However, new issue activity is now largely done for the year, and doesn’t typically pick up again until mid-to-late January, so if buying continues, look for secondary supply to tighten and for yields to edge lower–particularly if muni bond mutual fund redemptions slow down and take pressure off of the bid-side of the market.

As always, any major moves in Treasury yields will affect the muni yield curve as well. But reduced year-end liquidity and trading volumes could mean exaggerated market reactions to news, so be careful not to read too much in to any major changes in yields over the last trading days of the year.

The new year will bring with it increased headlines and speculation about the prospects for tax reform–a topic of keen interest to municipal bond investors. An article in Friday’s Wall Street Journal (The Looming Threat to Tax-Free Munis, link provided for subscribers) examines how lower tax brackets could reduce the value of the tax exemption for the tax-free income from munis. Lowering the top Federal rate from 39.6% to 33% (as Candidate Trump had proposed) would be unlikely to disrupt the muni market, but an alternative tax-reform proposal, which the author calls “the most radical” would lower the top rate on taxable bond interest to 16.5% and could have an effect on muni market values if enacted. Restricting the tax exemption of munis appears to be off the table, as the President Elect was quoted last week as being in favor of maintaining the tax exemption of munis.

Because the Trump proposal does not appear likely to have a severe impact on muni investors, it does not seem necessary to withhold new investments, but of course it does make sense to follow the debate next year.

Taxable Equivalent Yields at Different Current and Proposed Federal Income Tax Rates

| Muni Yield | 39.6% | 43.4% (39.6% + 3.8%) | 33% | 25% | 16.5% |

| 3% | 4.96% | 5.30% | 4.47% | 4.00% | 3.59% |

After Tax Yields at Different Current and Proposed Federal Income Tax Rates

| Taxable Yield | 39.6% | 43.4% (39.6% + 3.8%) | 33% | 25% | 16.5% |

| 4% | 2.41% | 2.26% | 2.68% | 3.00% | 3.34% |

Yield Trend: Longer munis underperformed last week, as can be seen by the larger increase in yields than was seen with Treasuries.

Fund Flows: While investors may have been stepping in to buy in the secondary market, muni bond mutual funds have continued to see large redemptions (below), which is part of the reason for the recent underperformance of the muni market. It is interesting to see that last week muni bond ETFs had positive inflows.

The Calendar

| 12/24 Saturday | Hanukkah begins | |

| 12/25 Sunday | Christmas Day | |

| 12/26 Monday | Christmas Observed | all U.S. markets closed |

| 12/30 Friday | Last Trade Date of the year | bonds close early |

| 1/16 Monday | Martin Luther King Holiday | all U.S. markets closed |

| 1/20 Friday at Noon ET | Inauguration of Pres. Trump | |

| 2/5 Sunday | Super Bowl 51 |

Here’s the link to the complete economic calendar on the MSRB’s EMMA website.

Muni Bond Market Data and Tables

The Bottom Line

Buy? Sell? Hold?

We favor low duration and high cash flow (premium) bonds in order to be able to maintain an appropriate asset allocation with minimal interest rate risk exposure.

Tax-Loss Swaps: We continue to encourage investors to consider realizing losses, especially from long-duration positions, but time is running out to get them done this year, as liquidity will likely decline as the week progresses. In order to maintain an appropriate asset allocation exposure, consider lower-duration solutions for the buy-side of swaps. Shorter duration muni ETFs can be used as a placeholder. See my article here for additional guidance on selecting a muni ETF.

Curve: The muni curve begins to flatten around the 10-year maturity range, but the interest rate risk at that spot of the curve may be a little bit too much, at least for the time being. Continue to favor the short end of your target maturity range.

Structure / Credit: Because of the risk of adverse tax consequences, avoid lower coupon bonds that would be at risk of getting priced at a discount if rates move a little higher. Favor premium bonds and good call protection. Because of the sell-off in the market and reduced dealer liquidity, some lower quality bonds have been trading at very attractive levels, but that reduced liquidity means that self-directed investors must do their homework carefully before buying a lower quality bond that may be difficult to sell in the future.

Thanks for Reading

Thank you for reading The Muni Catchup this year. The next edition is scheduled for the first week of the new year.

Best wishes for a holiday season that is bright with joy and rich with memories.

Peace be with you,

Pat

We use the AP Municipal Benchmark Curve, Powered by MBIS as our indicator of municipal market yields. The Associated Press (AP) – Municipal Bond Information Service (MBIS) U.S. Tax-Exempt Municipal Index covers the long-term tax-exempt municipal bond market and is based on actual trades and market quotes in the municipal bond market. The curve tracks the offered side of the market and includes smaller transaction sizes to reflect what individual investors may see in the market. The curve assumes 5% coupons with 10 year call protection. The curve is available to subscribers at http://www.mbis.com/apindex/ and is also distributed by The Associated Press to newspapers around the country.

This is not investment advice. The opinions expressed and the information contained herein are based on sources believed to be reliable, but accuracy or appropriateness is not guaranteed and are subject to change without notice. Past performance is interesting but is not a guarantee of future results. Investments in bonds are subject to gains/losses based on the level of interest rates, market conditions and credit quality of the issuer. Indices are not available for direct investment, although in some cases, there may be ETFs available designed to track some of the indices shown. The author does not provide investment, tax, legal or accounting advice. Investors should consult with their own advisor and fully understand their own situation when considering changes to their strategy, tactics or individual investments. Additional information available upon request.

©2016 Patrick F. Luby

All Rights Reserved