Portfolio Structure

Fixed Income Portfolio Structure: Bullet, Barbell or Ladder

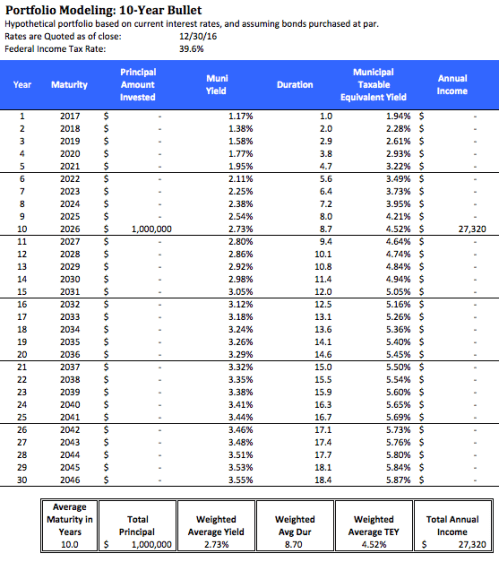

The Bullet Portfolio

The bullet portfolio has all of the assets concentrated in a single maturity date. The bullet portfolio may not be appropriate for investors who are sensitive to changes in the market value of their portfolios.

The Laddered Portfolio

A laddered portfolio has equal amounts of principal maturing each year throughout the life of the portfolio. A laddered portfolio is considered an interest rate neutral strategy, because it favors neither a rise nor a fall in interest rates.

Much as an equity investor can benefit from dollar-cost averaging, a bond investor can take advantage of changes in interest rates with a laddered portfolio. By having bonds rolling off on a regular basis—regardless of the interest rate environment—an investor may be able to avoid missing the opportunity of locking in attractive rates when yields are high, or having too much of a portfolio locked into low rates. For instance, with a 10-year laddered portfolio, 10% percent of the principal would be re-invested every year. If rates are low, the portfolio’s cash flow is insulated by the fact that ninety percent of the portfolio is locked up in rates higher than what is then available. If rates are higher, then the money rolling off can be invested at those higher rates.

Investors seeking to build a new laddered portfolio in a rising rate environment may wish to start by constructing a barbell, and redeploy principal as it matures to fill in the open maturities of the ladder.

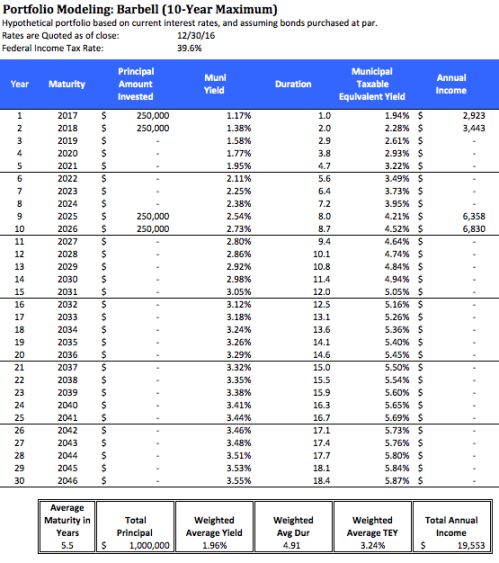

The Barbell Portfolio

Rather than having identical amounts of principal maturing every year as with a laddered portfolio, a barbell portfolio is heavily weighted toward the long and short ends of the maturity range.

Investors anticipating a rise in rates may prefer a barbell strategy (to a bullet strategy) because they may be able to reduce their portfolio volatility without having to liquidate all of the long bonds from their portfolio, thus being able to take advantage of the longer (and cheaper) sector of the muni curve without taking on too much interest rate risk. As rates move higher, some or all of the maturing short-term bonds can be reinvested in longer-term maturities—locking in higher rates.

Summary

Based on rates as of December 30, 2016, here are how three hypothetical “10-year” portfolios would have compared:

| Yield | Duration | Annual Income | |

| Bullet | 2.73% | 8.70 | $27,320 |

| Ladder | 1.99% | 5.05 | $19,858 |

| Barbell | 1.96% | 4.91 | $19,533 |

Note that the bullet portfolio has the highest duration and therefore the highest interest rate risk. Investors may prefer a bullet strategy when rates are declining in order to lock in more income and to take advantage of the price performance of the long duration bond.

The barbell has the lowest duration and slightly less income than the ladder. A barbell may be the preferred strategy when the yield curve is flattening–that is, when the difference between the short and long parts of the yield curve is moving lower, as when short-term rates are rising by more than long-term rates.

Investors who do not want to try to time interest rates may prefer the laddered portfolio strategy, as it favors neither a rising or falling interest rate environment. When rates are moving, a laddered portfolio is unlikely to be the best performing strategy, but it is also unlikely to be the worst performing strategy, and it is relatively easy to maintain.

This is not investment advice. This information is presented for informational purposes only. Any determination as to what bonds or strategy may be appropriate for you should reflect your own objectives and risk tolerance. The opinions expressed and the information contained herein is based on sources believed to be reliable, but its accuracy and appropriateness is not guaranteed. Past performance is interesting but is not a guarantee of future results. The author does not provide investment, tax, legal or accounting advice. Investors should consult with their own advisor and fully understand their own situation when considering changes to their strategy, tactics or individual investments. Investments in bonds and fixed-income investments are subject to gains/losses based on the level of interest rates, market conditions and changes in credit quality of bond issuers. Additional information available upon request.

©2017 Patrick F. Luby

All Rights Reserved