The Muni Catchup 1/30/17

This Week’s Ingredients:

This Week’s Ingredients:

- Chart of the Week

- Performance Snapshot

- Comments

- New Issue Supply

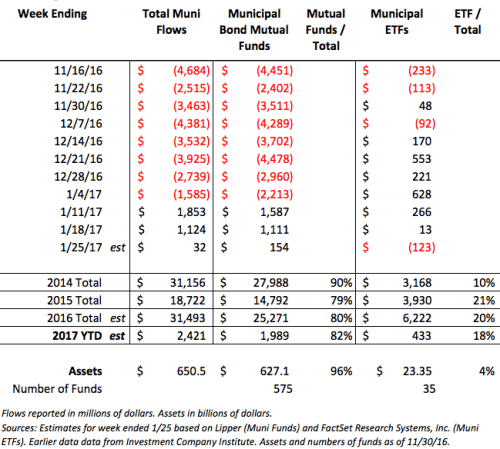

- Fund Flows

- Market Data

- The Calendar

- The Bottom Line

Chart of the Week

The chart above is from the January Miami Condo Market Snapshot by Andrew Stearns at StatFunding. The author writes:

From 2012 to mid-2015 Miami developers sold all units in each project within months of completion of the project. The inflection points of previous condo cycles have been marked by developers getting stuck with unsold developer units. The number of projects with unsold developer units is increasing.

Since the area is a gateway to Central and South America, was the market affected by the heightened prominence of immigration policy rhetoric in the presidential campaign? Will real estate markets such as South Florida, California and Hawaii be affected by this week’s executive order on immigration? If so, how might that filter though to state and local economic activity and tax receipts? It’s too early to tell, so this uncertainty has been added to our Muni Market Risk Radar.

(Hat tip to Nelson Rangel, CIO at Raven Capital B.V. for circulating the real estate report.)

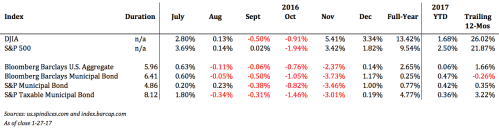

Performance Snapshot

Comments

Muni trading activity was brisk last week, with yields moving slightly higher. Overall muni bond fund flows remained positive, although muni ETFs turned in a slightly negative week–the first negative week in a little while. In other ETF news, the number of muni ETFs has grown: Virtus recently rolled out a new municipal bond ETF–ticker CUMB–subadvised by Cumberland Advisors. That brings the total number of muni ETFs to 36.

Last week, I attended the 10th annual Inside ETFs conference, along with more than 2,200 other people. While at the conference, I attempted an informal and non-scientific survey of advisors, to gauge their views on rates and how they position munis in their client portfolios.

Panel discussion on Infrastructure at Inside ETFs. (Brian Sully, Tortoise Index Solutions; Jodie Gunzberg, S&P Dow Jones Indices; Jeremy Held, ALPS Portfolio Solutions; Rich Cea, UBS Securities; Pat Luby, Income Investor Perspectives.)

While I had only a handful of conversations, I was surprised by the general perspective: even among a non-representative small number of advisors, all of whom were fiduciaries with an Investment Policy Statement for each of their clients, they were trying to time interest rates. It wasn’t expressed that way, of course, but in terms of managing risks. My parting counsel was my longstanding refrain, “Let your goals determine whether you include bonds in your portfolio. Let the market determine which bonds you buy.” There were a number of questions asked at the Inside ETFs fixed income sessions that were not able to be answered, so I will address some of them in next week’s Catchup.

Finally, in case you missed it, our latest article on muni ETFs, Using ETFs To Build A Sustainable Muni Portfolio was published last week on ETF.com.

Infrastructure

Can we come up with a better name than infrastructure? I am a very slow typist, and every time I have to type “infrastructure,” it takes me three times as long as it should, and it seems like I always have a typo. (I am grateful for spellcheck, though.)

Anyway, even though the topic has been pushed off the front page by other news from Washington, there appears to be a lot of action on the topic.

Reinforcing the need for infrastructure spending was the news of the failure of a structural support on the Delaware River Bridge, connecting New Jersey and Pennsylvania, forcing the temporary closure of the bridge. While the cause of the failure of the support appears to have been a construction error made sixty years ago, the situation illustrates the importance of spending on maintenance–the fracture was recent and was found during a routine inspection by engineers. (Kudos to the engineers for their diligence.)

While the National Governors Association has gathered a list of over 300 projects to consider for the President’s Federal infrastructure funding initiative, the Delaware Bridge closure demonstrates that not all infrastructure spending needs to be on shiny new projects–new projects that are funded must include some provision for ongoing maintenance, as appropriate. Otherwise, new projects–even if they are fully funded from Federal dollars, could add an additional drain on already stressed state and local governments. (Another item that has now been added to the Muni Risk radar.)

New on the Muni Risk Radar:

- State and local economic impact of changes to U.S. immigration policy

- Potential for new Federally funded infrastructure projects to add to state and local ongoing maintenance costs

New Issue Supply: Light week ahead…

- Last week: $6.8 billion

- This week: $3.9 billion

Click to see the complete New Issue Calendar on the MSRB’s EMMA site, which also allows you to see details on the new issues that have recently come to market.

Fund Flows: An up and down week…

Muni ETFs turned in the first negative week in over a month, while mutual funds continued their recent run of inflows–albeit at a much slower pace.

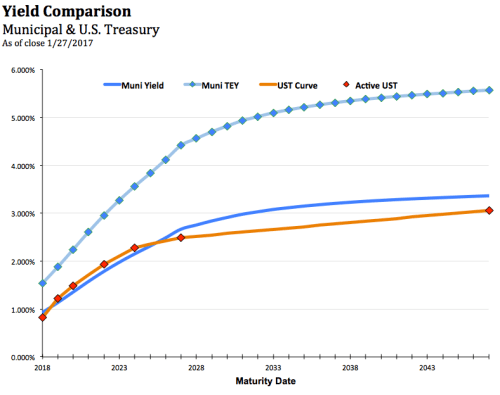

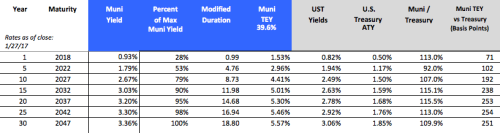

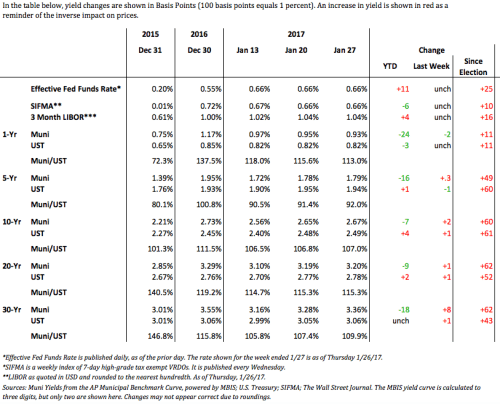

Market Data

The Calendar

- Economic Calendar

- Below are some other notable dates to keep on your radar:

| 1/31 – 2/1 | FOMC Meeting | no press conference |

| 2/5 Sunday | Super Bowl 51 | |

| 2/20 | Presidents Day Holiday | All U.S. markets closed |

| 3/14 – 3/15 | FOMC Meeting | With Press Conf. |

| 4/10 | DOL Fiduciary Rule | Scheduled to take effect |

| 4/14 | Good Friday | All U.S. markets closed |

| 4/18 Tuesday | Federal Tax Returns Due | Not on the 15th as usual |

| 5/2 – 5/3 | FOMC Meeting | |

| 5/29 | Memorial Day | All U.S. markets closed |

| 7/4 Tuesday | Independence Day | All U.S. markets closed |

| 9/4 | Labor Day | All U.S. markets closed |

| 10/9 Monday | Columbus Day | Stocks open / bonds closed |

| 11/11 Saturday | Veterans Day | Does not fall on a weekday |

| 11/23 | Thanksgiving | All U.S. markets closed |

| 12/25 Monday | Christmas | All U.S. markets closed |

| May, 14 2018 | Deadline for bond dealers to begin disclosing mark-ups on some bond trades | Effective date for new MSRB and FINRA rules. |

The Bottom Line

Buy? Sell? Hold? Ladder? Barbell? Bullet?

Structure: Barbell For investors building a portfolio from scratch, we favor a barbell now, with the expectation that it would be slowly converted to a ladder over the next 1 to 3 years.

Curve: We remain Cautious (underweight your duration target). Going too short on the curve and there is not enough yield to offset inflation, going too long on the curve and there is the potential double whammy of high duration (interest rate risk) combined with low liquidity.

Structure: Cautious We continue to favor premium bonds for protection from rising rates.

Credit: Cautious Perceptions of the economy and credit risk are going to be volatile in the months ahead as the new administration’s proposal are filled in. Municipal investors need to be very selective in taking on credit risk, especially from issuers with minimal margin of protection. The lower the credit quality, the greater the importance of liquidity, so when taking on more credit risk, be willing to take less than the maximum yield in order to be in a part of the market with more liquidity. As always, our preference for non-investment grade exposure is to use a professional manager via a SMA (Separately Managed Account) or mutual fund, or through an ETF which will offer very low costs and broad diversification.

And Now, a Word From Our Sponsor

If you or your firm are wondering about how to apply any of this to your conversations, please contact me. My specialty is helping advisors through the decision-making process of which muni bonds, funds, ETFs, CEFs or SMAs to consider for their clients. Click here for additional ideas about how you can take advantage of my expertise.

Thank you for reading, and best wishes for a great week,

Pat