Muni Catchup 10/17

by PL

Looking Back

Looking Back

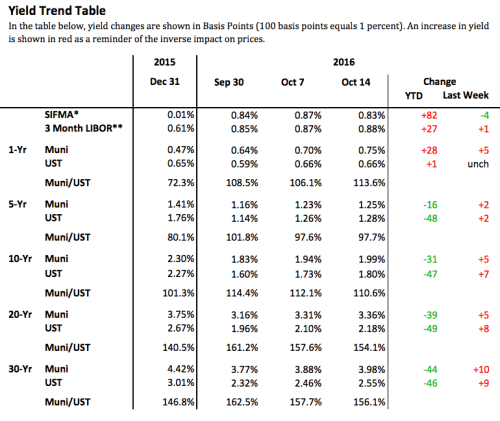

Bond market yields finished the week mostly higher, further eroding the year-to-date total returns for most indices. Nonetheless, if muni ETFs can be used as the bellwether, new money appears to be continuing to flow into the muni market. Weekly total net flows into muni ETFs increased to $150 million from $146 million in the prior week. (Estimated muni ETF flow data are available a week before mutual fund flow data are available. See the Context page for the flow data table.)

Looking Ahead

It is notable that just as the bond market is showing signs of weakness, a heavy slate of $15.4 billion in new issues is expected to be offered this week.

It is notable that just as the bond market is showing signs of weakness, a heavy slate of $15.4 billion in new issues is expected to be offered this week.

Part of what may be driving such heavy supply this week is that in the 11 weeks left in the year, four of them will be shortened by holidays (Veterans Day, Thanksgiving, Christmas and New Year’s), and a fifth week will have the election. Another possible driver of the timing of issuance may be the recent increase in yields–providing incentive for issuers to try to lock in at current rates.

While mutual fund flows have continued, the flows are dwarfed by the supply, so in order to attract sufficient buying interest, do not be surprised if new issue yields are cheapened in order to clear the market, creating some potential buying opportunities–particularly in the secondary market.

Market Wisdom

In accepting the Nobel Prize for economics, Economist Friedrich Hayek counseled being “apprehensive” regarding “the uncritical acceptance of assertions which have the appearance [emphasis Hayek’s] of being scientific.”

What looks superficially like the most scientific procedure is often the most unscientific, and, beyond this, that in these fields there are definite limits to what we can expect science to achieve. This means that to entrust to science – or to deliberate control according to scientific principles – more than scientific method can achieve may have deplorable effects.

“Friedrich August von Hayek – Prize Lecture: The Pretence of Knowledge”. Nobelprize.org.Nobel Media AB 2014. Web. 7 Dec 2014.

The entire speech is worthwhile reading for any investor or student of economics.

The Bottom Line

Curve: The cautious stance is re-emphasized, given the recent weakness in the bond market and the heavy new issue supply. For investors with new money to put to work or reinvest, favoring the shorter end of the maturity (or duration) target range can make sense.

Credit: Holding a modest amount of credit risk can add some incremental income as well as diversification. If the economy continues to improve and pushes rates higher, that should also tighten credit spreads, which could offset some of the duration risk. But as always, when thinking about adding non-investment grade bonds, consider hiring a professional manager–either through an SMA, mutual fund or an ETF.

Structure: Premium bonds remain favored for their lower duration and higher cash flow.

Calls: Beware of the total call risk in portfolios. If you are going to accept call risk, be sure that you are getting paid to do so.

Products: Muni bond mutual fund and ETF inflows continue to be positive. Favor lower duration solutions. There is a new muni ETF offering that investors can consider as well. MCEF from FirstTrust invests in muni bond closed-end funds, and may offer attractive yields, but beware of the high duration and therefore interest rate risk.

Sellers: Investors who will be selling should pay attention to the new issue calendar and the overall tone of the bond markets.

Have a great week, and thanks for reading. Let me know if you have any questions.

Pat

This is not investment advice. The opinions expressed and the information contained herein are based on sources believed to be reliable, but accuracy or appropriateness is not guaranteed and are subject to change without notice. Past performance is interesting but is not a guarantee of future results. Investments in bonds are subject to gains/losses based on the level of interest rates, market conditions and credit quality of the issuer. Indices are not available for direct investment, although in some cases, there may be ETFs available designed to track some of the indices shown. The author does not provide investment, tax, legal or accounting advice. Investors should consult with their own advisor and fully understand their own situation when considering changes to their strategy, tactics or individual investments. Additional information available upon request.

©2016 Patrick F. Luby

All Rights Reserved