Muni Catchup 10/24

by PL

This week in The Muni Catchup:

- Is The Muni Party Over?

- A look at trading flows, new issue supply and muni ETFs can offer some insight…

- Market Wisdom

- Are You Going to be in Newport Beach Next Month?

- The Bottom Line

Is The Muni Party Over?

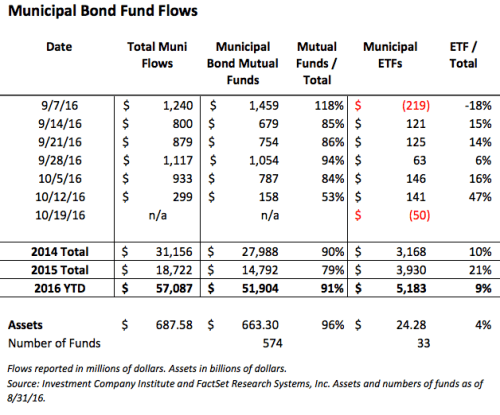

Last week, Lipper US Fund Flows estimated that for the week ended Wednesday October 19, muni bond mutual funds had net outflows of $27 million–that’s the first weekly net loss in assets in over a year. The Muni Catchup relies on the weekly data reported by The Investment Company Institute (ICI), which lags the Lipper data by a week. However, based on this week’s muni ETF flows (below), which were also negative, we expect that ICI will likely also report negative flows for the same period. See the Context page for additional data. Keep in mind, though, that 2016 flows already greatly exceed the flows of the last couple of years–suggesting that the flows are influenced by the aging demographics of the baby-boomers as their portfolios enter the de-accumulation phase and the need to generate investment income. Demographics won’t change as a result of changes in market sentiment.

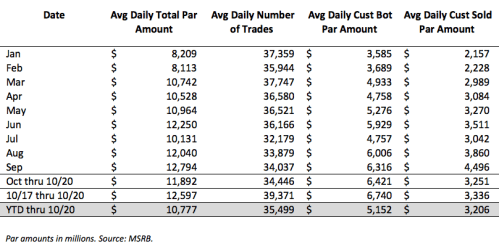

So does this mean that the muni party is over? Based the recent levels of trading activity, it doesn’t look like it:

Certainly, the recent very heavy new issue calendar has helped to drive trading activity, and will likely do so again this week with $16.5 billion expected to be priced.

But what should we read into the first week of negative muni fund flows in a year? There is a risk of over-analyzing these data or reading too much into them, but it can be helpful to look at what is going on with muni ETFs, because it is easier to summarize 35 ETFs than 574 open-end funds. If investors are indeed turning negative on municipals, then we might expect to see outflows across the entire universe of muni ETFs. On the other hand, if investors are reacting to an expected rise in interest rates, we should see flows out of longer duration ETFs and into shorter duration ETFs. The data below–sorted by duration–are from FactSet (via ETF.com) through October 20:

To summarize:

- The new issue calendar remains very heavy, suggesting that new issues may have to be priced “attractively” in order to clear the market

- Trading activity this month has been heavier than the YTD average

- ETF investors appear to be favoring shorter duration ETFs

- Year-to-date, most muni market total return indices are in positive territory, even though price action for the last several months has been negative

The party does not appear to be over, but participants appear to be taking a more cautious stance, rather than exiting munis. See The Bottom Line (below) for our thoughts on the implications.

Market Wisdom

I believe that to solve any problem that has never been solved before, you have to leave the door to the unknown ajar. You have to permit the possibility that you do not have it exactly right.

From The Meaning of It All, by Richard P. Feynman, winner of the 1965 Nobel Prize in Physics.

While Feynman made this comment in a lecture on the uncertainty of science, I believe that it also applies to investing. Because the objectives and risk tolerances of every investor are unique, the planning and implementation processes are solving for a goal that has not been solved before, so there must be an allowance for the possibility that “you do not have it exactly right.” In practical terms, that is why the regular review of objectives and the portfolio are so important.

Are You Going to be in Newport Beach Next Month?

You know, for the world’s largest fixed income ETF conference? If so, please let me know in advance so we can say “hello.” If you haven’t made plans yet, it’s not too late.

In addition to hearing other fixed income luminaries, you can hear me present “The Case For Muni Bonds: Active vs. Passive In The Puerto Rico Era.”

Click here to see the complete agenda or to reserve a seat.

The Bottom Line

Curve: We re-emphasize our cautious stance. Even with last week’s slight price improvement, the recent weakness in the bond market and the heavy new issue supply and growing expectations for a December rate hike from the Fed combine to encourage an underweight in duration. (For the sake of comparison, based on current rates and assuming par bonds, a 15-year laddered muni portfolio would have a duration of 7.1, and a 10-year ladder would have a duration of 5.2.)

The heavy supply may create some opportunities for investors to pick up some attractively priced bonds both in the primary and secondary market, but with the cautious stance, we remind readers to not stretch for yield–set your duration target to the lower end of your range and seek out the best available combination of risk and yield.

Credit: Holding a modest amount of credit risk can add some incremental income as well as diversification. If the economy continues to improve and pushes rates higher, that should also tighten credit spreads, which could offset some of the duration risk. But as always, when thinking about adding non-investment grade bonds, consider hiring a professional manager–either through an SMA, mutual fund or an ETF.

Structure: Premium bonds remain favored for their lower duration and higher cash flow.

Calls: Beware of the total call risk in portfolios, and watch out for extension risk with bonds priced to a call.

Products: Muni bond mutual fund and ETF inflows have dwindled and may remain negative in the weeks ahead, putting pressure on market prices and on NAVs.

Have a great week, and thanks for reading. Let me know if you have any questions.

Pat

This is not investment advice. The opinions expressed and the information contained herein are based on sources believed to be reliable, but accuracy or appropriateness is not guaranteed and are subject to change without notice. Past performance is interesting but is not a guarantee of future results. Investments in bonds are subject to gains/losses based on the level of interest rates, market conditions and credit quality of the issuer. Indices are not available for direct investment, although in some cases, there may be ETFs available designed to track some of the indices shown. The author does not provide investment, tax, legal or accounting advice. Investors should consult with their own advisor and fully understand their own situation when considering changes to their strategy, tactics or individual investments. Additional information available upon request.

©2016 Patrick F. Luby

All Rights Reserved

[…] party may not be over, but it appears to be getting much more subdued. In last week’s Catchup, we noted that Lipper reported an end of the year-long muni inflow party. They reported that for […]

LikeLike