Muni Catchup 10/31

by PL

Nope! The Party’s Not Over!

The party may not be over, but it appears to be getting much more subdued. In last week’s Catchup, we noted that Lipper reported an end of the year-long muni inflow party. They reported that for the week ended Wednesday October 19, muni bond mutual funds had net outflows of $27 million–the first weekly net loss in assets in over a year. For the week ended October 26, Lipper reported a net inflow of $256 million. (They report only on muni bond mutual funds–not muni bond ETFs.) The authoritative ICI data always lags Lipper by a week, but preliminary data for muni ETF flows shows a return to positive flows after last week’s net outflows.

Lipper and ICI use different methods to calculate their reports, but the takeaway is not who’s got the numbers exactly right, because they are both reporting a slowdown in flows. The more interesting questions are about the cause, and what investors should be doing.

Likely (or possible) causes: strengthening economy (see Friday’s GDP report) and increasing expectation for a post-election rate hike from the Fed.

What should investors be doing? While the decline in flows suggests that some investors are allocating out of munis, for individual investors, a change in asset allocation is generally appropriate when there is a change in goals or situation–not a change in the market. A change in market conditions can be more appropriately reflected in a change in security selection or risk exposure. In other words, a change in duration or credit risk exposure. It would make us feel better if the muni fund flows showed assets moving within the investment class rather than exiting…that suggests some investors trying to time rates, which is notoriously difficult.

See The Bottom Line, below, for more specific thoughts.

Supply

This week’s new issue supply is expected to be only the single-digit billions, which should take some pressure off the market.

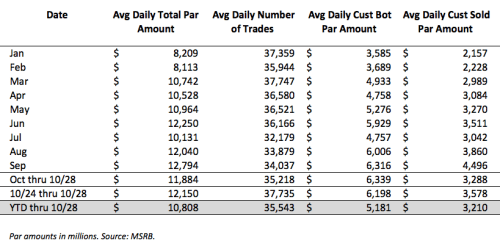

Trading Activity

Last week’s trading activity was higher than the month-to-date average–not surprising given the extremely heavy new issue activity. Notice, though, that the pace of customer buying is below the pace of the month–also not surprising, given the slackening flows into funds and growing expectations of a Fed rate hike soon.

Market Wisdom

The shorter a portfolio’s duration, the more frequently maintenance is required.

From Managing a Family-Fixed Income Portfolio by Aaron S. Gurwitz.

Portfolio maintenance adds to costs–so shortening duration to reduce interest rate risk is not a cost-free solution for portfolios. Because of the likelihood of higher security turnover, consider using a muni ETF for temporary low duration exposure.

The Calendar

There’s always a lot on the calendar, so the trick is paying attention to the couple of things that may not be on the calendar or that may be overlooked. There are 9 weeks left in the year, and 4 of those weeks will be “impaired”: affected by holidays and/or major events: such as election day or market holidays. Below is the link to the complete economic calendar, and here are some key events to keep in mind:

| 11/1 & 2 Tue & Wed | FOMC meets | |

| 11/2 & 3 Wed & Thu | Inside ETFs: Inside Fixed Income 2016 | |

| 11/6 Sunday | End of Daylight Savings | |

| 11/8 Tuesday | Election Day | |

| 11/11 Friday | Veterans Day | stocks open / bonds closed |

| 11/24 Thursday | Thanksgiving Day | all U.S. markets closed |

| 12/13 & 14 Tue & Wed | FOMC meets | |

| 12/25 Sunday | Christmas Day | |

| 12/25 Sunday | Chanakuh begins | |

| 12/26 Monday | Christmas Observed | all U.S. markets closed |

| 12/30 Friday | Last Trade Date of the year | bonds close early |

Here’s the link to the complete economic calendar on the MSRB’s EMMA website.

The Bottom Line

While some of the supply pressures have eased this week, the upcoming partial weeks will also likely reduce new issue supply. However, investors will be distracted by the election and then focused on the potential post-election impact on the markets. Caution remains the watch word.

Curve: favor the shorter end of your duration range.

Credit: the economic numbers suggest an improving economy, but it is premature to “load up” on credit. A modest exposure to credit risk is a good diversifier, however. Exposure to non-investment grade credit risk should be for no more than 10% of the fixed income allocation and should be done using full-time professional management, such as an SMA, mutual fund or ETF.

Structure: continue to favor premium bonds, but pay attention to portfolio level exposure to call risk and the potential for bonds that are currently priced to the call to get priced to maturity if rates move higher–which would increase duration risk. (This is called extension risk.)

Products: slowing flows into funds will reverberate throughout the market. Do not chase recent performance! Select funds or SMA strategies based on how the objective fits with the investor’s goals.

Thanks!

Thanks for reading! Have a great week.

Pat

This is not investment advice. The opinions expressed and the information contained herein are based on sources believed to be reliable, but accuracy or appropriateness is not guaranteed and are subject to change without notice. Past performance is interesting but is not a guarantee of future results. Investments in bonds are subject to gains/losses based on the level of interest rates, market conditions and credit quality of the issuer. Indices are not available for direct investment, although in some cases, there may be ETFs available designed to track some of the indices shown. The author does not provide investment, tax, legal or accounting advice. Investors should consult with their own advisor and fully understand their own situation when considering changes to their strategy, tactics or individual investments. Additional information available upon request.

©2016 Patrick F. Luby

All Rights Reserved