Muni Catchup 11/7

by PL

Last week:

Last week:

- Yields down / prices up

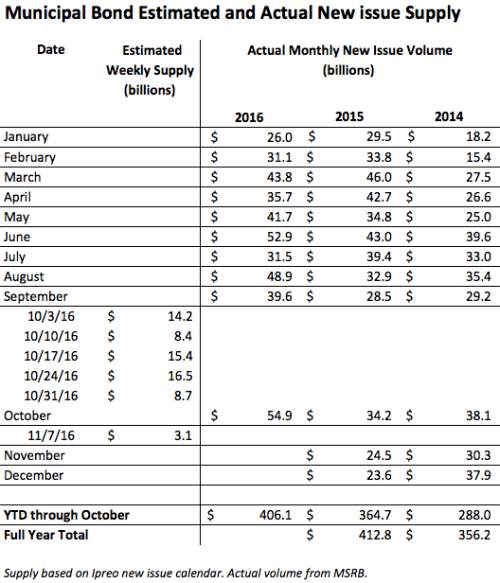

- Heavy supply closing in on a record

- Uptick in muni ETF flows

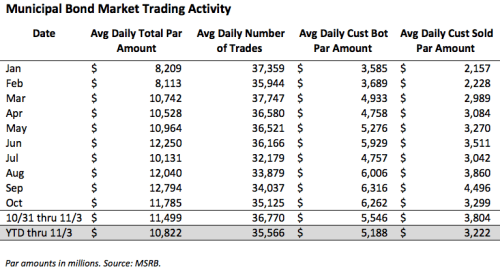

- Customer buying below recent trend / selling slightly above average

This week:

- Election + Veterans Day Holiday (Friday)

- Tiny new issue calendar

Plus:

- Market Wisdom

- The Bottom Line

*SIFMA is a weekly index of 7-day high-grade tax exempt VRDOs. It is published every Wednesday.

**LIBOR quoted in USD, as of Thursday 11/3/16.

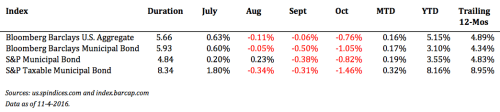

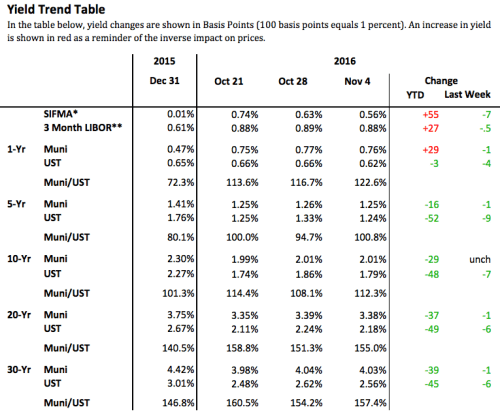

Benchmark muni yields moved lower last week, influenced no doubt by the volatility in the equity markets. As a result, most total return indices–after several weeks of negative performance–were positive for the week. The price improvements came in spite of customer buying activity that was below recent averages and selling that was up slightly; however, demand would have been helped by the slight uptick in flows into muni ETFs last week.

After another week of heavy new issue supply, the week ahead will be unusually light–good thing, too, with the election and the bond market expected to be closed on Friday. Nonetheless, total new issue volume for the year is close to eclipsing last year’s total, and could surpass the record volume of $433 billion, set in 2010.

The Calendar

U.S. bond markets are scheduled to be closed on Friday in observance of Veterans Day.

| 11/8 Tuesday | Election Day | |

| 11/11 Friday | Veterans Day | stocks open / bonds closed |

| 11/24 Thursday | Thanksgiving Day | all U.S. markets closed |

| 12/13 & 14 Tue & Wed | FOMC meets | |

| 12/25 Sunday | Christmas Day | |

| 12/25 Sunday | Chanakuh begins | |

| 12/26 Monday | Christmas Observed | all U.S. markets closed |

| 12/30 Friday | Last Trade Date of the year | bonds close early |

Here’s the link to the complete economic calendar on the MSRB’s EMMA website.

Market Wisdom

The first principle is that you must not fool yourself–and you are the easiest person to fool.

From Surely You’re Joking Mr. Feynman!, by Richard Feynman.

Believe it or not, this book by the Nobel Prize winning physicist Richard Feynman is laugh-out-loud funny. I was prompted to re-read it last week after my friend Barnet Sherman mentioned that he always assigned the last chapter of this book (“Cargo Cult Science”) to interns and new employees. After re-reading the chapter, I decided to re-read the whole book. The chapter and the book are both highly recommended.

The Bottom Line

Supply pressures will be way down, but with the election, demand pressure will also very likely be way down. Caution remains the watch word.

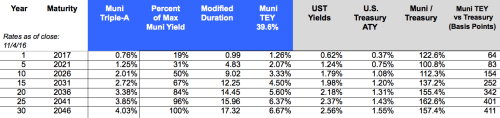

Curve: favor the shorter end of your duration range. While the 13-year spot on the muni curve captures about 60% of the max yield available, a 13-year par bond would have a duration of about 11. Going out to 16-years should capture about 70% of the max yield–but duration there would be around 12.6. In comparison, a 10-year ladder right now (assuming high-grade par bonds) would have a duration of about 5.2, while a 15-year ladder would have a duration of 7.1.

Credit: the economic numbers suggest an improving economy, but it is premature to “load up” on credit. A modest exposure to credit risk is a good diversifier, however. Exposure to non-investment grade credit risk should be for no more than 10% of the fixed income allocation and should be done using full-time professional management, such as an SMA, mutual fund or ETF.

Structure: continue to favor premium bonds, but continue to pay attention to portfolio level exposure to call risk and the potential for bonds that are currently priced to the call to get priced to maturity if rates move higher–which would increase duration risk.

Products: fund flows (into mutual funds and ETFs) are slower than they have been, but remain positive. Do not chase recent performance, but choose funds or SMA strategies based on how the objective fits with the investor’s goals.

Thanks!

Thank you for reading! Have a great week.

Pat

This is not investment advice. The opinions expressed and the information contained herein are based on sources believed to be reliable, but accuracy or appropriateness is not guaranteed and are subject to change without notice. Past performance is interesting but is not a guarantee of future results. Investments in bonds are subject to gains/losses based on the level of interest rates, market conditions and credit quality of the issuer. Indices are not available for direct investment, although in some cases, there may be ETFs available designed to track some of the indices shown. The author does not provide investment, tax, legal or accounting advice. Investors should consult with their own advisor and fully understand their own situation when considering changes to their strategy, tactics or individual investments. Additional information available upon request.

This is not investment advice. The opinions expressed and the information contained herein are based on sources believed to be reliable, but accuracy or appropriateness is not guaranteed and are subject to change without notice. Past performance is interesting but is not a guarantee of future results. Investments in bonds are subject to gains/losses based on the level of interest rates, market conditions and credit quality of the issuer. Indices are not available for direct investment, although in some cases, there may be ETFs available designed to track some of the indices shown. The author does not provide investment, tax, legal or accounting advice. Investors should consult with their own advisor and fully understand their own situation when considering changes to their strategy, tactics or individual investments. Additional information available upon request.