Muni Catchup 11/14

by PL

Oh! That’s Gonna Leave a Mark!

As the U.S. equity market zoomed higher last week, U.S. bond prices moved sharply lower. For example, the yield on the 10-year Treasury Note moved higher by 36 basis points, while the 30-year Treasury Bond moved higher by 38 basis points. (There are 100 basis points in 1 percent.)

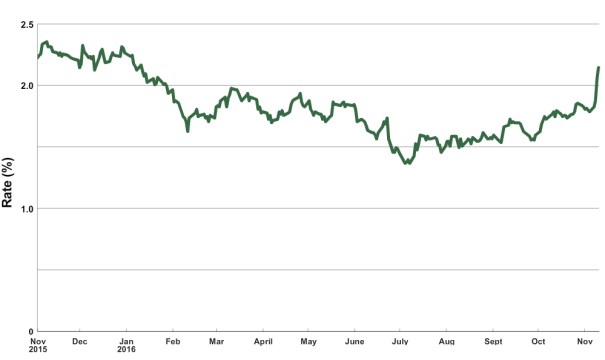

Daily close of the 10-year U.S. Treasury Note.

While 10 and 30-year Treasuries are still lower in yield on the year, they are well above the low yield mark for the year–the 10-year, which closed last week at 2.15% hit 1.37% on July 5. The price declines just in the last week will have a significant effect on the market in a couple of ways:

- Traders will be looking to protect their trading profits for the year (and therefore their bonuses), and will be very cautious in the few weeks remaining in the year–potentially reducing liquidity even more.

- Investors have slowed their buying pace in the past couple of weeks (see the Fund Flows and Trading Activity as indicators), and are unlikely to aggressively jump in unless yields stabilize or continue to move higher and get to some “round” numbers. A market that simply “drifts” to higher yields will make it difficult to attract investors.

Here is some insight from this week’s Barron’s:

You heard it here first: Jeffrey Gundlach, CEO of DoubleLine Capital and one of the world’s most successful bond investors, predicted in January at the Barron’s Roundtable that Donald J. Trump would be the country’s next president, noting, “The populist momentum is unstoppable.”

Now that the New York businessman has shocked much of the world by vanquishing rival Hillary Clinton, Gundlach sees something else unstoppable: a rise in bond yields that could lift the yield on the 10-year Treasury note to 6% in the next four or five years.

Trump’s pro-business agenda is inherently “unfriendly” to bonds, Gundlach says, as it could to lead to stronger economic growth and renewed inflation. Gundlach expects President-elect Trump to “amp up the deficit” to pay for infrastructure projects and other programs. That could produce an inflation rate of 3% and nominal growth of 4% to 6% in gross domestic product. “If nominal GDP pushes toward 4%, 5%, or even 6%, there is no way you are going to get bond yields to stay below 2%,” he says.

“Gundlach: Bond Yields Could Hit 6% in Five Years,” by Lauren R. Rubin, Barron’s. November 12, 2016. Barron’s subscribers can link to the article here.

While 6% is a long way from current rates, a steady climb to 6% over 5 years could still result in positive total returns in the interim, albeit well below what we have seen recently.

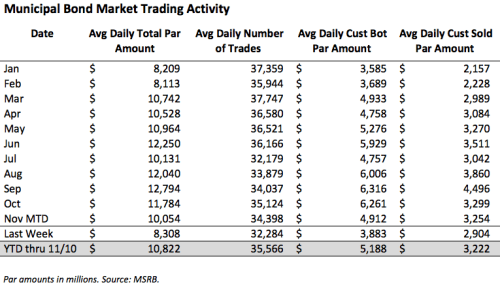

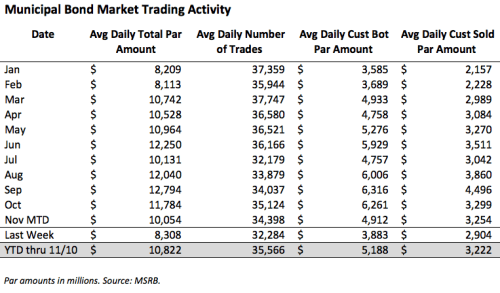

Unsurprisingly, municipal bond market trading volume was down last week, with the average daily par amount traded and customer buying both down. Customer selling was also down.

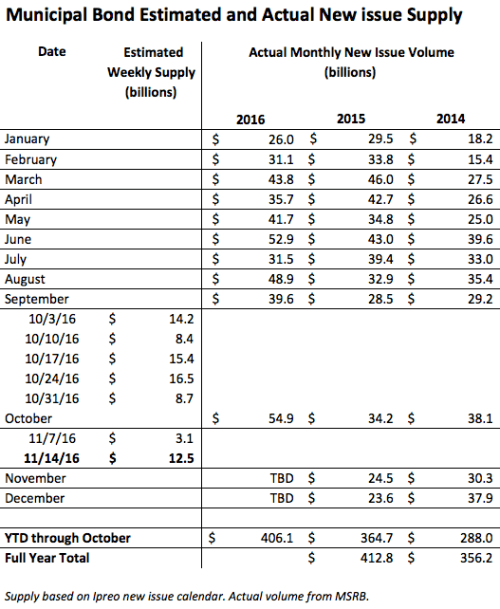

At $12.5 billion, the new issue calendar for this week is heavy–but do not be surprised if deals are delayed, given the dramatic upturn in rates, and decline in trading activity.

Liquidity Update

A letter from the Executive Director of the Municipal Securities Rulemaking Board (MSRB) to the Securities and Exchange Commission identified several areas that could pose a potential risk to retail investors in the municipal bond market. One of the concerns cited was the decline in the number of dealers:

The number of dealer firms in the municipal market continues to decline, which contributes to shrinking inventories. Since October 2012, the number of MSRB-registered dealers is down by 19 percent. This decrease is a result of both the exit of registered dealers from the market, as well as mergers and acquisitions and other consolidation of dealer firms. The combination of a reduction in the dealer population, a decrease in dealer holdings and increasing municipal bond mutual fund balances could lead to reduced liquidity in the municipal market. This type of market dislocation could have a significant impact on mutual fund net asset value (NAV) and the overall value of investors’ municipal bond positions.

Letter from Lynnette Kelly, Executive Director of the MSRB to the SEC. November 3, 2016.

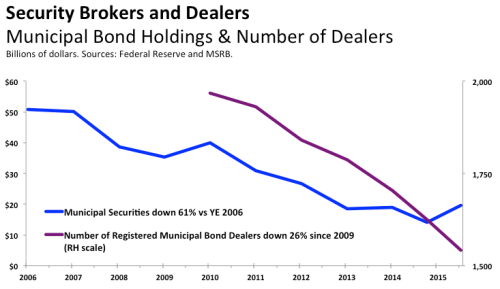

Most municipal market investors and their advisors would agree that liquidity in the municipal bond market has declined in the last several years. Since the end of 2006, the estimated amount of broker/dealer assets devoted to supporting the municipal bond market has declined by over 60%.

The reduction of broker/dealer support of the municipal bond market is not surprising, as the trend reinforces the anecdotal observations about the changing nature of secondary market liquidity. (This chart is not intended to imply complete precision in the amount of capital deployed by the broker/dealer community to the markets, but rather to be indicative of the trend of their level of activity in the markets.)

The recent reduction of support of the market by broker/dealers has created a tangible reduction in the ability of investors to easily sell or buy on a consistent basis. While this does not mean that investors should reduce or avoid municipal bond investments solely for this reason, it does raise the importance of considering potential secondary market liquidity prior to making any investment decisions.

Self-directed investors must be comfortable with the implications for their own portfolios, or consider if they would prefer delegating portfolio decisions to a professional manager.

Important Note: Change in Data Source

Beginning this week, we are now using the AP Municipal Benchmark Curve, Powered by MBIS as our indicator of municipal market yields. The Associated Press (AP) – Municipal Bond Information Service (MBIS) U.S. Tax-Exempt Municipal Index covers the long-term tax-exempt municipal bond market and is based on actual trades and market quotes in the municipal bond market. The curve tracks the offered side of the market and includes smaller transaction sizes to reflect what individual investors may see in the market. The curve assumes 5% coupons with 10 year call protection. The curve is available to subscribers at http://www.mbis.com/apindex/ and is also distributed by The Associated Press to newspapers around the country.

Reply Hazy Try Again Later

Wow. What a week. Are interest rates ready to turn the corner? Even the trusty Magic 8-Ball isn’t helpful in here. (“Replay hazy try again.”)

Click here for an extended full-page version of the Yield Trend Table showing quarter-by-quarter changes. Suitable for framing or wrapping fish.

The Calendar

| 11/24 Thursday | Thanksgiving Day | all U.S. markets closed |

| 12/13 & 14 Tue & Wed | FOMC meets | |

| 12/25 Sunday | Christmas Day | |

| 12/25 Sunday | Chanakuh begins | |

| 12/26 Monday | Christmas Observed | all U.S. markets closed |

| 12/30 Friday | Last Trade Date of the year | bonds close early |

Here’s the link to the complete economic calendar on the MSRB’s EMMA website.

Market Wisdom

Most stories about investors ruined in the market are stories about lack of diversification.

DollarLogic, by Andy Martin.. Page 195.

The bond market volatility will no doubt send some investors to the sidelines and headline writers to their thesauruses to come up with ever more hyperbolic ways to elicit fear and negativity about bonds. But keep in mind that the pursuit of long-term goals needs a long-term perspective and a diversified portfolio. Last week provided a good example of that–equities did well while most bonds were down. Market conditions should influence the choice of specific investments or strategies, but the asset allocation mix should be determined by the investor’s goals.

The Bottom Line

Demand pressure has been down, and supply pressure could be up this week (maybe). Caution remains the watch word.

Curve: favor the shorter end of your duration range. If the portfolio is overweighted in duration, consider adding very low duration positions to balance long duration holdings. Adding an ETF to an all-bond portfolio can be an effective and quick way to get that done. See my recent article on the topic here.

Credit: the economic numbers suggest an improving economy, but it is premature to “load up” on credit. A modest exposure to credit risk is a good diversifier, however. Exposure to non-investment grade credit risk should be for no more than 10% of the fixed income allocation and should be done using full-time professional management, such as an SMA, mutual fund or ETF.

Structure: continue to favor premium bonds, but be sure to pay attention to portfolio level exposure to call risk and the potential for bonds that are currently priced to the call to get priced to maturity if rates move higher–which would increase duration risk.

Products: fund flows (into mutual funds and ETFs) have slowed dramatically. Do not chase recent performance, but choose funds or SMA strategies based on how the objective fits with the investor’s goals.

Let’s Be Careful Out There!

Thanks for reading, have a great week.

Pat

This is not investment advice. The opinions expressed and the information contained herein are based on sources believed to be reliable, but accuracy or appropriateness is not guaranteed and are subject to change without notice. Past performance is interesting but is not a guarantee of future results. Investments in bonds are subject to gains/losses based on the level of interest rates, market conditions and credit quality of the issuer. Indices are not available for direct investment, although in some cases, there may be ETFs available designed to track some of the indices shown. The author does not provide investment, tax, legal or accounting advice. Investors should consult with their own advisor and fully understand their own situation when considering changes to their strategy, tactics or individual investments. Additional information available upon request.

©2016 Patrick F. Luby

All Rights Reserved