Muni Catchup 1/17

This Week’s Ingredients:

- Commentary

- Chart of the Week

- Performance Snapshot

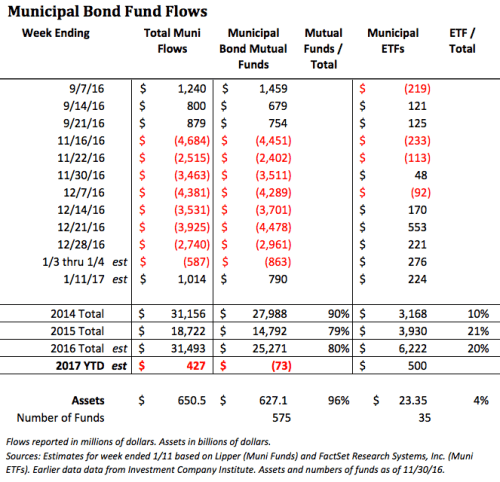

- Fund Flows Turn Positive

- New Issue Supply Picking Up

- The Calendar

- Market Data

- The Bottom Line

Commentary

- Municipal bond fund flows turned positive last week for the first time since early November

- New issue volume ticked up a little last week, and is expected to be at full-speed this week

- Secondary market trading volume last week was fairly heavy for so early in the year–average daily trading volume of $11.8 billion was higher than last year’s daily average of $11.1 billion and well over the $9.1 billion for the first full trading week of January 2016

- Market activity remains focused on the short to intermediate parts of the muni market, with only 32% of last week’s trading volume in bonds due in 20-years or more. (According to MSRB trading data.)

Headlines continue to accrue about problems and concerns about underfunded public pension liabilities. In our view, MOST of these problems will be played out in slow motion, so self-directed investors and fiduciaries will need to be vigilant in their credit surveillance. As the market digests the headlines, there may be opportunities to pick up incremental yield, but diligent credit analysis and surveillance will be the critical because while it can be nice to earn a fatter yield, holding too long can have a big downside.

This is what S&P had to say about state finances in a recent report:

Credit pressure across the U.S. state sector is likely to remain elevated throughout 2017 as slow tax revenue growth compounded by growing pension contribution requirements and Medicaid expenditures is contributing to fiscal strain for many states.

And, their comments on local finances:

Stability and resiliency are two longstanding credit features of the local government sector. In 2017 both of these factors will be extremely important as municipalities grapple with a range of budgetary challenges.

And a real-world example from Chicago Mayor Rahm Emmanuel who has asked Moody’s not to rate an upcoming bond issue:

As City Hall prepares to borrow $1.2 billion, Mayor Rahm Emanuel has asked a Wall Street debt ratings agency that’s been highly critical of Chicago’s finances to withdraw its evaluation of city creditworthiness, the administration disclosed Tuesday.

The mayor contends that the junk status placed on the city’s debt by Moody’s Investors Service drives up borrowing costs covered by taxpayers and does not reflect the steps he has taken to fix the city’s finances.

Ratings are an important data point for advisors and investors, but not enough on which to base the investment decision, especially for challenged credits where prudence now demands experienced forward-looking judgement about credit risk, political risk and valuation. Hence the increasing need for independent analysis and the growing value of professional management.

Keep in mind that borrowers do not have a fiduciary obligation to lenders, and that bond buyers can rely only on the contractual agreement that secures the bonds. To lend a borrower money for 10, 20 or 30 years requires some sense that the strength of that agreement will remain as stong (or stronger) in the years ahead. No doubt buyers will fully subscribe the Chicago bond issue, but even for those who will not be buyers and students of the market, it provides an interesting story–perhaps a cautionary tale.

Did you read the Muni Catchup from January 3rd? If not, I highly recommend it, especially for advisors, because it includes a list of almost 20 municipal bond market risk factors that you may not have thought of, but which I think are important to be watching. If you are an advisor preparing for client conversations, you may wish to pair that with our article on The Benefits of Professional Management. If you would like customized versions of either or both of these pieces, my contact information is here.

By the way, a lot of readers see The Muni Catchup on LinkedIn and Twitter, but if you subscribe to e-mail updates (which are free of charge and spamless), you would have seen the risk list already.

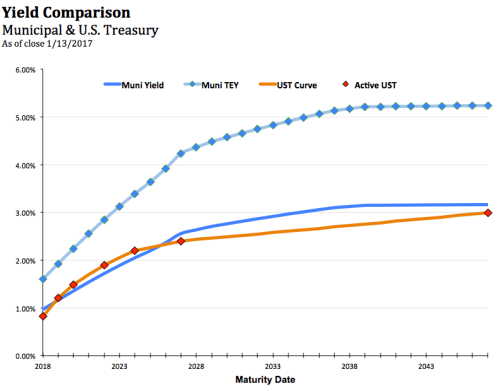

Chart of the Week

Not only has the 5-year spot in the muni market declined rapidly, it has done so with increasing trade volume.

Performance Snapshot

Index junkies and number crunchers should visit S&P Dow Jones Indices Municipal Bond Page for additional performance data.

Fund Flows Turn Positive

After 8 consecutive weeks of outflows, mutual funds finally had a week of net inflows. Interestingly, over the same 9 weeks, muni ETFs only had 3 weeks with negative flows.

New Issue Supply Picking Up

- Last week: $8.7 billion

- This week: $9.5 billion

Click to see the complete New Issue Calendar on the MSRB’s EMMA site, which also allows you to see details on the new issues that have recently come to market.

Calendar

- Economic Calendar

- Below are some other notable dates to keep on your radar:

| 1/20 Friday at Noon ET | Inauguration of Pres. Trump | |

| 1/22 – 1/25 | Inside ETFs | Will you be there? |

| 1/31 – 2/1 | FOMC Meeting | |

| 2/5 Sunday | Super Bowl 51 | |

| 2/20 | Presidents Day Holiday | All U.S. markets closed |

| 3/14 – 3/15 | FOMC Meeting | With Press Conf. |

| 4/10 | DOL Fiduciary Rule | Scheduled to take effect |

| 4/14 | Good Friday | All U.S. markets closed |

| 4/18 Tuesday | Federal Tax Returns Due | Not on the 15th as usual |

| 5/2 – 5/3 | FOMC Meeting | |

| 5/29 | Memorial Day | All U.S. markets closed |

| 7/4 Tuesday | Independence Day | All U.S. markets closed |

| 9/4 | Labor Day | All U.S. markets closed |

| 10/9 Monday | Columbus Day | Stocks open / bonds closed |

| 11/11 Saturday | Veterans Day | Does not fall on a weekday |

| 11/23 | Thanksgiving | All U.S. markets closed |

| 12/25 Monday | Christmas | All U.S. markets closed |

| May, 14 2018 | Deadline for bond dealers to begin disclosing mark-ups on some bond trades | Effective date for new MSRB and FINRA rules. |

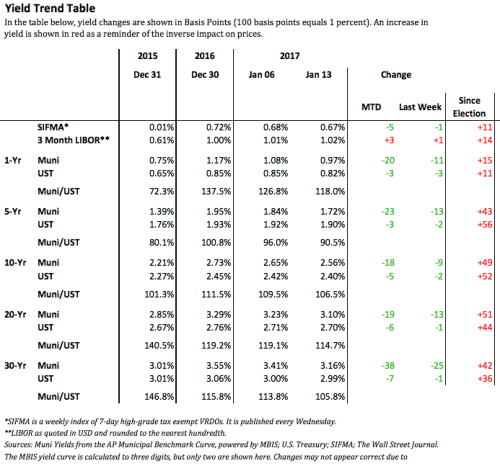

Market Data

The Bottom Line

Buy? Sell? Hold? Ladder? Barbell? Bullet?

Readers already know our views on timing the market, so the questions about buy, sell and hold don’t generally apply for investors (as opposed to traders looking for tactical opportunities). The real question should be overweight (because valuation is cheap and buyers are earning more than usual for the risks involved), underweight (valuation is rich and risks are being under-compensated) or neutral weight (valuation and risk compensation are neutral).

Structure: Barbell For those who need a refresher about the differences between a ladder, barbell and bullet portfolio structures, see our Glossary. For investors building a portfolio from scratch, we favor a barbell now, with the expectation that it would be slowly converted to a ladder over the next 1 to 3 years.

Curve: Cautious Going too short on the curve and there is not enough yield to offset inflation, going too long on the curve and there is the potential double whammy of high duration (interest rate risk) combined with low liquidity. As can be seen in the graph above, there is a turn in the curve beyond ten years, where incremental duration risk receives much less incremental reward. We have never been in favor of arbitrarily drawing a line at ten years as some investors do, so if there are opportunities to pick up attractive amounts of incremental yield by extending a few years beyond 2028, that may be worth considering.

Structure: Cautious We continue to favor premium bonds for protection from rising rates pushing holdings into a market discount (which can accelerate the decline in market value, due to the onerous tax treatment of market discount that exceeds the “de minimis” exclusion).

Credit: Cautious Perceptions of the economy and credit risk are going to be volatile in the months ahead as the new administration’s proposal are filled in. Municipal investors need to be very selective in taking on credit risk, especially from issuers with minimal margin of protection. The lower the credit quality, the greater the importance of liquidity, so when taking on more credit risk, be willing to take less than the maximum yield in order to be in a part of the market with more liquidity. As always, our preference for non-investment grade exposure is to use a professional manager via a SMA (Separately Managed Account) or mutual fund, or through an ETF which will offer very low costs and broad diversification.

And Now, a Word From Our Sponsor

If you or your firm are wondering about how to apply any of this to your conversations, please contact me. My specialty is helping advisors through the decision-making process of which muni bonds, funds, ETFs, CEFs or SMAs to consider for their clients. Click here for additional ideas about how you can take advantage of my expertise.

And be sure to let me know if you will be at Inside ETFs next week so we can say hello.

Thank you for reading, and best wishes for a great week,

Pat