Muni Catchup 12/5

This Week in The Muni Catchup:

- Yields and Buying are Up

- Fund Flows: Mutual Funds Negative but ETFs Positive (slightly)

- New Issue Supply Remains Heavy, but…

- The Bottom Line

- Muni Data Tables and Charts

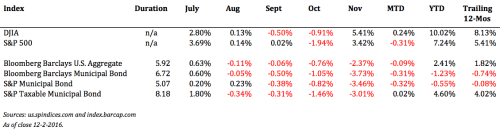

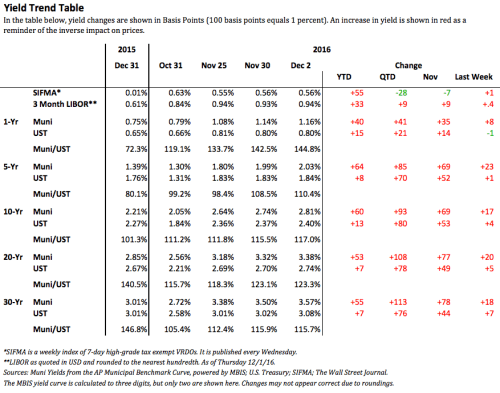

Muni market yields continued to move higher last week (see the Yield Trend table, below) but the higher yields appeared to draw attention from buyers, as the average daily par amount bought jumped over the prior week. Granted, the week before was distorted by the Thanksgiving holiday, but customer buying activity was heavier than the current seasonal (post Labor Day) average (see the Trading Activity Table, below). A week does not necessarily mean a new trend is emerging, but it does appear that yield starved investors are taking advantage of the higher yields.

Meanwhile, although customer selling has been above average, it is somewhat surprising that it has not been heavier, as the increase in yields (and decline in market values) may present an opportunity for investors to execute tax-loss swaps to harvest capital losses and reposition their portfolios. (See The Bottom Line, below, for more on this topic.)

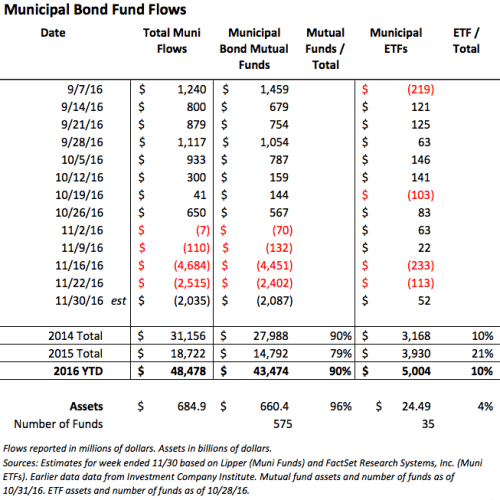

Fund flows last week were a mixed bag–mutual fund flows remain heavily negative, while muni ETFs had a slightly positive week. Since many investors will be receiving their November month-end statements in the coming days, seeing the drops in muni bond mutual fund NAVs may lead to further redemptions.

The new issue calendar is heavy again this week, but as the end of the year gets closer, new issue supply will decline, taking pressure off of the supply side of the market–if demand continues, look for the muni market to get firmer. This week’s new issues are likely to be “priced to move,” as issuers and underwriters will be anxious to clear the market as quickly as possible. As providers of liquidity, investors with cash to put to work may wish to be on the lookout for attractively priced new issuers.

By the way, if you don’t know that T.S. Eliot was wrong, that means that you missed the November market recap. Here’s the link to it so you can go read it now.

The Bottom Line

Is this a buying opportunity? Or should investors be selling?

Yields have moved higher very quickly, so while we generally remain cautious, current levels do appear to present a buying opportunity. However, investors are cautioned to not extend too far out the yield curve unless they are comfortable with the duration. This is particularly important for investors in mutual funds and ETFs which have a duration target–while long-term holders will ultimately benefit from new higher rate bonds cycling into the funds, the NAVs may be pressured if rates continue to move higher.

Tax-loss swaps: Consider realizing losses, especially from long-duration positions. In order to maintain an appropriate asset allocation exposure, consider lower-duration solutions for the buy-side of swaps. Shorter duration muni ETFs can be used as a placeholder. See my article here for additional guidance on selecting a muni ETF.

Curve: Favor the shorter-end of your maturity range. Keep in mind that even though we have seen a sharp upward move in rates, it is possible that the market could reverse and rates could rally, so it is important to both maintain the appropriate asset allocation and also to pay attention to call features so that if rates do rally, bonds do not get called away.

Structure / Credit: With reduced liquidity in the market and the approach of year-end, it makes sense in here to “pay up” for a more liquid bonds: favor single-“A” or better premium bonds. For exposure to lower quality bonds, use a professionally managed vehicle such as a mutual fund, ETF or separately managed account (SMA).

Muni Data Tables and Charts

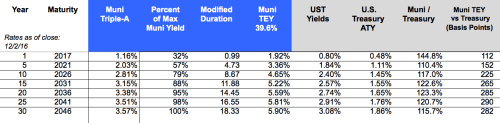

We are now using the AP Municipal Benchmark Curve, Powered by MBIS as our indicator of municipal market yields. The Associated Press (AP) – Municipal Bond Information Service (MBIS) U.S. Tax-Exempt Municipal Index covers the long-term tax-exempt municipal bond market and is based on actual trades and market quotes in the municipal bond market. The curve tracks the offered side of the market and includes smaller transaction sizes to reflect what individual investors may see in the market. The curve assumes 5% coupons with 10 year call protection. The curve is available to subscribers at http://www.mbis.com/apindex/ and is also distributed by The Associated Press to newspapers around the country.

Thanks For Reading

If you do not already subscribe, you should do so right now. There are several special articles planned for the weeks ahead that you will not want to miss. The subscription form is below. As a reminder, there is no charge for The Muni Catchup, but if you find it helpful, you can help me by sharing it.

Have a great week,

Pat

This is not investment advice. The opinions expressed and the information contained herein are based on sources believed to be reliable, but accuracy or appropriateness is not guaranteed and are subject to change without notice. Past performance is interesting but is not a guarantee of future results. Investments in bonds are subject to gains/losses based on the level of interest rates, market conditions and credit quality of the issuer. Indices are not available for direct investment, although in some cases, there may be ETFs available designed to track some of the indices shown. The author does not provide investment, tax, legal or accounting advice. Investors should consult with their own advisor and fully understand their own situation when considering changes to their strategy, tactics or individual investments. Additional information available upon request.

©2016 Patrick F. Luby

All Rights Reserved